| S&P BSE Sensex* |

Re/US $ |

Gold Rs/10g |

Crude ($/barrel) |

FD Rates (1-Yr) |

38,090.64 |-299.18

-0.78% |

72.16 |-0.21

-0.29% |

30,478.00 | -57.00

-0.19% |

79.12 |2.55

3.33% |

5.00% - 7.00% |

Weekly changes as on September 12, 2018

BSE Sensex value as on September 14, 2018

Impact

Are Indian bonds becoming unattractive investment options? Looks like it.

Over the last six months, RBI has hiked policy rates twice, aggregating to a 50 basis point (bps).

Rising bond yields aren’t a pleasant sight for investors.

Through the FY 2018-19, the yield on India’s 10-year benchmark bond, 7.17% (2028), has surged nearly one percentage point, i.e. 100 bps. Bond prices share a negative co-relation with bond yields and interest rates.

Will investors take a calculated risk to invest in debt funds now, expecting yields to soften a bit?

Or will they keep off debt funds?

Before you decide on this, it’s imperative for you to assess the present bond market conditions thoroughly.

Let’s begin the assessment…

(Image source: maxpixel.net)

Why bond yields are rising in India lately?

-

Federal Reserve in the U.S. has been resolute on hiking the interest rates even in future. The U.S. monetary policy tightening in the U.S. is pushing bond yields up not only in the U.S. but also across the world. Experts have been anticipating at least two more rate hikes in 2018 and perhaps three in 2019.

-

A strong US dollar (US$) and rising yields in the U.S. have caused a sell-off in emerging market bonds and weaker currencies. Millions of dollars had flown to emerging markets in search of better returns during the time of quantitative easing. Now, this trade is reversing. Currency turmoil in Turkey and Argentina have made the pack of emerging markets even more unattractive for global investors. India is no exception to this trend.

-

Although the retail inflation fell to 3.69%––a 10-month low in August 2018, there are clearly upside risks. Rising crude oil prices and higher Minimum Support Prices (MSPs) announced by the government on crops are likely to push inflation further up.

-

Many experts believe, the Indian Rupee (INR) is overvalued at present, even after factoring in the current fall. Falling INR and rising crude oil prices is a lethal combination for India. It might deteriorate India’s Current Account Deficit (CAD) position. In Q1 FY 2018-19, India recorded a CAD of 2.4% of GDP which is a tad lower than 2.5% recorded a year ago during same period. Remittances helped India avoid a hard landing. Nonetheless, the Balance of Payment (BoP) situation of India worsened in Q1, FY 2018-19. Against the surplus of US$ 11.4 billion in Q1 FY 2017-18, there was a deficit of US$ 11.3 billion in Q1, FY 2018-19. However, rising crude oil prices and a jump in non-oil, non-gold imports would be a cause of concern, going forward.

-

RBI’s average daily liquidity infusion stood at Rs 4,700 crore between May 2018 and July 2018. In April 2018 the average daily infusion was only about Rs 240 crore. The differential between weighted average call rates and repo rate has fallen sharply in the July and August 2018, indicating that the days of easy liquidity are over. This has sent yields on the short-tenure bonds northwards.

-

RBI has refrained from intervening excessively in the forex market to contain the slide of INR. In other words, RBI is allowing INR to depreciate until it erases its relative overvaluation against the broader basket of global currencies. This has caused a sentiment-driven sell-off in INR, which in turn resulted in hardening of bond yields.

-

Since RBI is keeping off the heavy interventions in the forex, curtailing inflation has become even more crucial to maintain the country’s competitiveness. Else, depreciating INR will result in higher CAD, and higher inflation might take its toll on domestic growth. Some market participants are of the view that the RBI might have to hike policy rates further. Rising bond yields have factored in this fear from time to time. RBI will announce its fourth bi-monthly monetary policy statement for 2018-19 on October 04, 2018.

-

Although the central government is determined about containing fiscal deficit below 3.3% of GDP in FY 2018-19, the deficit, by end of July, touched 86.5% of the full-year estimate. It’s possible that some expenses were front-loaded and some incomes will accrue in months to come. Still, the government will find it difficult to curtail fiscal deficit, especially given the upcoming Lok Sabha Elections.

A positive perspective…

Foreign Institutional Investors (FIIs) hold less than 5% of total outstanding debt in India. That makes us less vulnerable to sudden outflows on account of unforeseen global events. The domestic-driven nature of Indian bond markets works to its advantage; especially when, the INR is falling sharply and the RBI isn’t enthused to artificially support it beyond a point.

So, what should be your strategy to invest in debt funds at this juncture?

Selecting the right category of debt mutual funds is crucial.

PersonalFN is of the view that, one should still be very careful and cautious while investing at the longer end of the yield curve. To put it simply, investing in long-term debt funds (holding longer maturity debt papers) can be risky in the foreseeable future.

Currently, shorter maturity papers are more attractive and fund houses, too, are aligning their portfolios accordingly.

Ideally, you’ll be better off if you deploy your hard-earned money in short-term debt funds; but ensure you’re giving due importance to your investment time horizon, asset allocation, and diversification.

Consider investing in short-term debt funds for an investment horizon of upto 2 years.

If you have an investment horizon of less than 1 year, low duration and money market funds would be the preferred choice.

And if you have an extremely short-term time horizon (of less than 6 months), you would benefit from investing in liquid funds and ultra-short duration funds.

Remember that investing in debt funds is not risk-free.

[Read: 5 Facets To Look Into While Investing In Debt Mutual Funds]

A few highly rated corporate deposits and bonds may also yield better returns than bank FDs. But make sure you study the company’s financials before investing, as the risk of default can’t be ignored. This will save you from financial shocks. Recently, a few banks too have increased their deposit rates, so do take note.

[Read: Factors To Look At While Investing In Bank FDs]

If you are investing in debt funds right now, you can’t afford to close your eyes to the reality. Bond yields are rising, Net Asset Values (NAVs) of debt funds are taking a knock on ratings downgrade and India’s currency is in a free fall.

Rather than being optimistic, being vigilant will pay off at this juncture.

Editor’s note:

Vigilant investors need vigilant advisors.

Your search for the most personalised investment advice might end at ‘PersonalFN Direct’—PersonalFN’s robo advisory platform. It is India’s only robo advisor powered by solid research experience.

But, how is it different from other robo advisory platforms?

#1: It offers only DIRECT PLANS (devoid of commissions)

#2: Offers customisable investment solutions based on your risk profiling

#3: It brings outstanding research experience of over 15 years

#4: Minimal paperwork and ease of transacting

#5: It comes at a pocket-friendly price

Investing in mutual funds through PersonalFN Direct is simple, rewarding, and economical. To know more, click here.

What are you waiting for?

Become a paid subscriber of PersonalFN Direct today and start your journey towards wealth creation.

Happy Investing!

Investors Are Redeeming From Equity Mutual Funds Now. Should You?

Impact

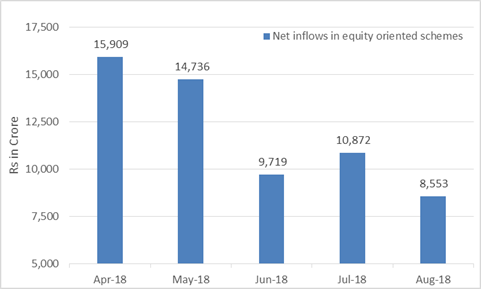

Is the party for mutual funds over?

In April 2018, the mutual fund industry received new monthly inflows of Rs 15,909 crore for all equity-oriented schemes combined. By August 2018, however, the net monthly inflows reduced 46% to Rs 8,553 crore.

What's making mutual funds unpopular nowadays?

The equity-oriented schemes include equity funds, arbitrage funds, equity-oriented hybrid funds and Equity Linked Savings Schemes (ELSS)

Data as on August 31, 2018

(Source: AMFI, PersonalFN Research)

And net inflows in pure equity-oriented mutual fund schemes dropped for the fifth month straight as on August 2018. That has started worrying some industry players.

In fact, net monthly inflows in equity-oriented funds are ebbing because of higher redemptions.

Is this just a momentary blip, or an indication of a major change for the mutual fund industry? And more importantly, how is this shift going to affect your investments?

Let's discuss this…

As on July 31, 2018, the industry has recorded a rise in mutual fund accounts for the 50th month. Moreover, investments through Systematic Investment Plans (SIPs) also increased. Data from the Association of Mutual Funds in India (AMFI) suggests that on an average 9.92 lakh new SIP registrations were activated every month (upto July) in FY 2018-19.

Therefore, it's very unlikely that mutual funds will become unpopular anytime soon. Investors have been rational to take the SIP route to invest in mutual funds.

To read more, please click here.

How IL&FS Rating Downgrade Will Impact Your Mutual Funds…

Impact

Casualties are inevitable in “too-big-to-fail” organisations when they find themselves in hot water.

And when mutual fund houses invest in debt instruments issued by such companies, thousands of investors suffer.

Recently, Net Asset Values (NAVs) of several mutual fund schemes took a knock in the range of 0.1% to 1.2%.

Mind you, mutual fund houses incurred these losses effectively in a day. They had to mark down their investments in Infrastructure Leasing & Financial Services (IL&FS) and its group companies owing to credit rating downgrades.

As per data obtained from ACE MF, nearly 14 mutual fund schemes collectively had an exposure of Rs 2,130 crore to IL&FS and its group companies as on August 31, 2018.

Astonishingly, liquid funds and ultra-short term debt funds such as Principal Cash Management Fund and Principal Ultra-Short Term Debt Fund suffered 1.2% and 1.0% loss respectively between September 07 and September 10.

To read more, please click here.

Tutorials:

Can Fixed Deposits Help You Retire Comfortably?

7 Investment Avenues for Your Post-Retirement Portfolio

Financial Terms. Simplified.

Interest Rate Risk:

The interest rate risk is the risk that an investment's value will change due to a change in the absolute level of interest rates, in the spread between two rates, in the shape of the yield curve, or in any other interest rate relationship. Such changes usually affect securities inversely and can be reduced by diversifying (investing in fixed-income securities with different durations) or hedging (such as through an interest rate swap).

(Source: Investopedia)

Quote:"The best business returns are usually achieved by companies that are doing something quite similar today to what they were doing five or ten years ago.”‒Warren Buffett