(Image source: Image by Gerd Altmann from Pixabay)

(Image source: Image by Gerd Altmann from Pixabay)

The Department of Posts under the Ministry of Communications & IT issued revisions in the rule for PPF, SCSS, and PO Savings Scheme. These amendments pertain mainly to the power of the sanctioning authority in the case of claims made on the demise of the first account holder where there is no nomination or legal evidence.

The revised rule stated below will come into force, with immediate effect:

"The authorities mentioned below are competent to sanction claims without production of legal evidence up to the limit noted against each, after expiry of Six (6) Months from the date of death of the depositor, if no succession certificate or probate of will or letter of administration of the deceased estate is produced during the period or up to the date of sanction."

Table 1: The sanctioning limit for the respective authorities

| Sl.No |

Name of Authority |

Limit in (Rs.) |

| (i) |

Time Scale Departmental Sub- Postmasters |

5,000 |

| (ii) |

Sub Postmasters in Lower Section Grade/PM Grade-1 |

10,000 |

| (iii) |

Sub- Postmasters/ Deputy Postmasters/ Postmasters in Higher Selection Grade (all Non Gazetted)/ PM Grade- II and III |

25,000 |

| (iv) |

Deputy Postmasters/ Senior Postmasters/ Deputy Chief Postmasters/ Superintendent of Post Offices/ Deputy Superintendent of Post Offices (All Gazetted Group -B) |

1,00,000 |

| (v) |

Chief Postmasters in GPO/ Head Offices, Senior Superintendent of Post Offices (All Gazetted Group -A) |

2,50,000 |

| (vi) |

Director HQ/Regional Directors/ Directors (GPO) |

3,75,000 |

| (Vii) |

Chief Postmasters General/ Postmasters General |

5,00,000 |

(Source: utilities.cept.gov.in)

On May 20, 2019, there was an order passed about certain amendments to the POSB(CBS) Manual Volume I & II with regards to the change in powers of various authorities to sanction deceased claim cases and their time-line in respect of Post Office Savings Schemes, including Certificates, where no nomination has been registered and there is no legal evidence available or produced.

Further, another order was sanctioned on August 29, 2019 clarifying the sanctioning limit for the respective authorities to be applicable for PPF and SCSS.

Until now, legal heirs, if they were not registered as nominee/s for any post office scheme of the deceased, they had to provide a succession certificate to claim the money. If they failed to do so, the money was kept in the post office as unclaimed.

Now with the new applicable revised rules, certain post office authorities have been given the power to sanction the claim amounts; even in cases where the succession certificate or probate of will or letter of administration of the deceased estate has not been produced by the claimants. This has been done to make the process seamless.

As per the circular, this rule is applicable to all the core banking solutions (CBS) and non-CBS post offices. Furthermore, it states that in the case where claims are not yet submitted or claims are submitted but not yet sanctioned, these revised provisions should be made applicable.

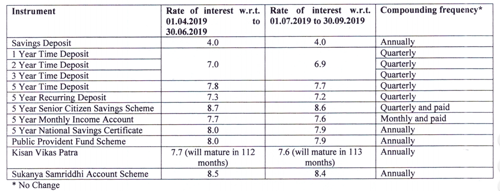

However, this is not the only amendment in the small saving schemes offered by the government for investment. For the second quarter of Financial year, 2019-20, there was a rate cut on small saving schemes of 10-basis points put into effect from 1st July 2019, till 30th September 2019.

This was proposed by the Finance Ministry, headed by Ms Nirmala Sitharaman, with the intent to reduce the cost of capital and increase the lending activity to boost the economy. Besides the Savings deposit, every other small saving scheme, including KVP and Sukanya Samriddhi scheme, too had a rate cut of 10 basis point.

[Read: The Impact Of Interest Rate Cut In Small Saving Schemes On You]

Table 2: Revised Interest rates for small saving schemes

(Source: Department Of Economic Affairs)

This was proposed because the banks didn't transmit this rate cut to the retail investors nor did they reduce their lending rates; since the RBI made 25 basis point rate cuts, successively, in the past three monetary policy committee meetings held and took an accommodative stance. But this didn't bolster the revival of the economy.

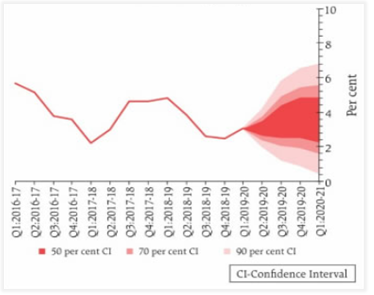

On the contrary, in the last third bi-monthly RBI monetary policy meeting held on August 7, 2019, the members of the committee, looking at the benign CPI inflation and lower 'core inflation' readings took a collective decision to cut policy rates by another 35 bps (departing from the normal practice of 25 bps) from 5.75 per cent to 5.40 per cent to support growth amidst concerns of weak demand.

Further, the MPC decided to maintain the 'accommodative monetary policy stance'. It was done with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4.00% within a band of +/- 2.00% while supporting growth.

Plus in terms of Liquidity concerns, the weighted average call money rate (WACR) - the operating target of monetary policy - was aligned with the policy repo rate in June, but it traded below the policy repo rate on a daily average basis by 14 bps in July and 17 bps in August (up to August 6, 2019).

The transmission of policy repo rate cuts to the weighted average lending rates (WALRs) on fresh rupee loans of banks has improved marginally since the last meeting of the MPC. Overall, banks have reduced their WALR on fresh rupee loans by 29 bps during the current easing phase from February to June 2019.

But the real CPI inflation has been muted, as observed from various high frequency indicators that suggest weakening of both domestic and external demand conditions.

[Read: Why A Slowdown in GDP Matters To You As An Investor?]

Graph 1: RBI's Quarterly CPI inflation projections

(Source: Third Bi-monthly Monetary Policy Statement)

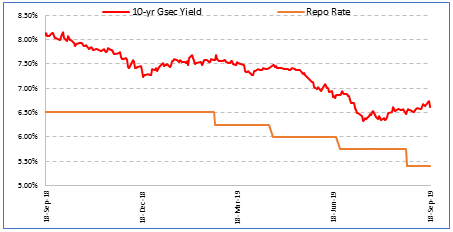

Private consumption, the mainstay of aggregate demand and investment activity remained sluggish. The MPC has noted that inflation is currently projected to remain within the target over a 12-month time horizon. The past rate cuts are being gradually transmitted to the proletariat economy with several banks reducing their fixed deposits rates further. Even the 10-Year Benchmark Yield slipped from 8.10% on September 18, 2018 to 6.62% on September 18, 2019.

Graph 2: Movement of 10 yr Gsec yield and repo rate for last one year

Data as of September 18, 2019

(Source: RBI, PersonalFN Research)

And the current 6-year low economic growth shows the benign inflation outlook prevails may provide headroom for policy action to close the negative output gap.

Although many actions were announced to boost the economy, they have remained dismal, so it's probable another rate cut is being hinted at. But contrary to RBI's expectations, if CPI inflation moves up beyond its comfort zone or medium-term inflation target of 4.0%, the scope for a further policy rate cut from RBI reduces.

Many Indians still find these government saving schemes as attractive investments because they provide a higher rate of return than the bank FDs despite the rate cut. But going forward, the gains in these may be limited and will not help in creating wealth for you in times of rapid inflation. This is because the interest income earned is taxable and might be not as appealing.

So, be sensible and have an astute investment strategy that will help you create wealth and one that stands in good stead for your long-term financial well-being.

[Read: Are You Paying Attention To Your Financial Fitness?]

This article first appeared on Certified Financial Guardian.

Add Comments