(Image source: Image by Deedster via Pixabay)

(Image source: Image by Deedster via Pixabay)

Along with the onset of monsoons last week, another wave hit the finance sector - the rate cut on small saving schemes. The 10-basis point expected rate cut implemented by the Finance Ministry, headed by Ms Nirmala Sitharaman, is done with the intent to reduce the cost of capital and increase the lending activity to boost the economy.

Since the RBI made 25 basis point rate cuts successively in the past three monetary policy committee meetings, to push the repo rate at 5.75%, the banks didn't budge and transmit this to the retail investors or reduce their lending rates. The RBI in the latest monetary policy meeting, held in June even changed the stance to accommodative from neutral to achieve the medium-term target for consumer price index (CPI) inflation of 4 per cent inflation and to boost the subdued GDP.

[Read: Why A Slowdown in GDP Matters To You As An Investor?]

(Source: RBI Minutes of the Monetary Policy Committee Meeting June 3, 4 and 6, 2019)

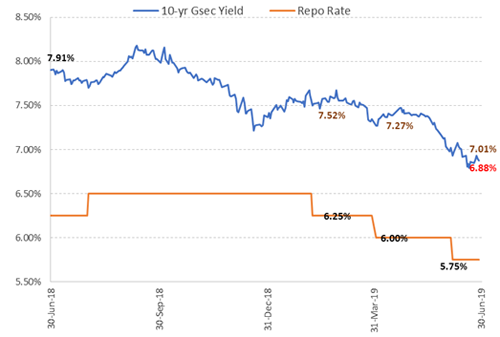

The 10-Year Benchmark Yield in G-Sec slipped from 7.91% on June 29, 2018 to 6.88% (marked in red) on June 28, 2019 within a year. After the RBI made the successive 25 basis point rate cut in repo rate, the 10-year benchmark G-sec has been dipping (marked in brown) and the 10-bps cut on small saving schemes dragged the index to 6.88%.

Graph: Impact of rate cuts on the movement of 10-year G-sec yield

Data as of June 28, 2019

(Source: RBI, PersonalFN Research)

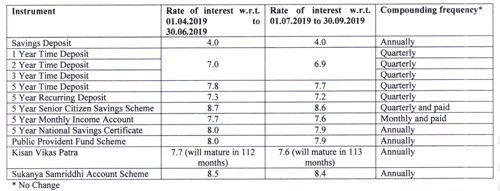

The government notifies about the interest rates of small saving schemes on a quarterly basis, and for upcoming July to September quarter, the finance ministry took a stand of reducing the policy rates. Besides the Savings deposit, every other small saving scheme, including KVP and Sukanya Samriddhi scheme, has been cut by 10 basis point.

Table 1: Revised Interest rates for small saving schemes

(Source: Department Of Economic Affairs)

The overall economy had witnessed a liquidity crunch, thereby impacting the consumer sentiment and current GDP reflects the low demand. Despite the repo rate cut, banks didn't proceed seamlessly and effectively to pass it down to retail investors and even to borrowers. Instead, the retail banks always pointed out that the interest rates offered by the government on small saving schemes have been attractive and better than the bank FD rates.

Hence in a move to match the softening of interest rates in the banking sector with the repo rate cut of RBI, and to reduce the borrowing costs so that they are passed on to the consumers, the expected cut came into effect from July 1, 2019 in order to push spending and economic activity.

From the excerpt of Bharatiya Janata Party's 2019 election manifesto, "In the last five years, we re-imposed macro-economic stability while building lasting frameworks for economic governance. These frameworks include the Insolvency & Bankruptcy Code, inflation-targeting, nationwide Goods & Services Tax, and the banking sector clean-up. These efforts have not only changed the business culture of the country and anchored inflation at 4 percent but have also been internationally recognized with a sovereign rating upgrade and a sharp rise in our Ease of Doing Business ranking. We will ensure that India remains the world's fastest growing major economy in future while maintaining macro stability. We aspire to be the world's third largest economy by 2030." It is evident that the government aims to control the inflation and boost economy.

Many Indians still find these government saving schemes as attractive investments for they provide a higher rate of return than the bank FDs despite the rate cut.

But the question is can this reduced rate cut help in creating wealth for you in times of rapid inflation?

If you will ask me, it may not provide you with real inflation-adjusted returns.

[Read: How To Improve Your Return On Investments?]

Investing in equities does help in creating wealth if you remain invested for a longer time period. But there is extreme risk involved. And investing in debt instruments, considered to be safe, the biggest delusion, has opened investors eyes wide open due to the debacle of downgrading of corporations.

So, the only way to earn better returns is to opt for mutual funds as it offers diversification to mitigate the risk emanating from both asset classes. Besides Mutual Fund investing takes into cognisance an investor's risk appetite, financial goals and investment time horizon; it is professionally managed by an expert.

When you invest in mutual funds, it offers you an opportunity to make a financial plan that involves an investment strategy to create an optimum and robust portfolio to achieve your goals.

Depending upon whether you are an aggressive, moderate, or conservative investor, you can structure the portfolio astutely to an equity fund, debt fund, and gold fund to own a robust diversified portfolio. Plus to counter the market volatility and avoid timing the market, opt for Systematic Investment Plans (SIPs). Moreover, investing in direct plans helps you accelerate your returns for your blissful future.

Consider the following asset allocation of equity funds depending on the type of investor you are.

Table 2: Indicative asset allocation for various investor type in current times.

| Portfolio Type |

(Aggressive) |

(Moderately Aggressive) |

(Moderate) |

(Moderately Conservative) |

(Conservative) |

| Large Cap |

0% to 10% |

10% to 20% |

20% to 30% |

20% to 30% |

30% to 40% |

| Large & Midcap |

10% to 20% |

10% to 20% |

10% to 20% |

0% to 10% |

|

| Midcap |

30% to 40% |

20% to 30% |

10% to 20% |

|

|

| Multi Cap |

20% to 30% |

20% to 30% |

20% to 30% |

20% to 30% |

10% to 20% |

| Value Style |

|

0% to 10% |

10% to 20% |

20% to 30% |

20% to 30% |

| Small Cap |

10% to 20% |

0% to 10% |

|

|

|

| Aggressive Hybrid |

|

|

10% to 20% |

20% to 30% |

20% to 30% |

(For illustration purpose only)

To build a solid portfolio of actively managed mutual fund schemes, choose them based on various quantitative and qualitative parameters.

Before you invest in mutual funds, it is necessary to check the following:

-

Your/Investor's risk profile.

-

Your investment objective.

-

Your financial goals.

-

The time horizon you have before goals befall.

Editor's Note: Do you want to invest in worthy mutual funds that will help you accomplish your financial goals?

Consider PersonalFN's credible flagship research service - Fundselect, that enters in its 20th Year.

It is an unbiased research service that provides insightful guidance and recommendations on equity funds and debt schemes. As a part of our Special Pre-Anniversary Offer, we are offering you, dear reader, "Fundselect".

Subscribe NOW to invest in some of the most reliable schemes available for your long-term wealth creation!

Happy Investing!

Add Comments

| Comments |

press123@gmail.com

Apr 02, 2020

Now a days Intt. Rates on Bank Deposits/FD ; as well as Post office Schemes have gone down drastically there by Denting Heavily on the Sr.Citizens Monthly Income. Share Markets & Mutual Funds have Become Much more Rickey.

What is the Best Option left for aged Sr. Citizens to Earn Risk Free minimum 9-10 % Intt. / year (before tax) on long term bases.. |

1