History of Indian taxation is deep rooted as old as 2300, years old. The current tax system is based largely on the ancient tax system of maximum social welfare found in the ancient scriptures of Manusmriti and Arthshashtra.

History of Indian taxation is deep rooted as old as 2300, years old. The current tax system is based largely on the ancient tax system of maximum social welfare found in the ancient scriptures of Manusmriti and Arthshashtra.

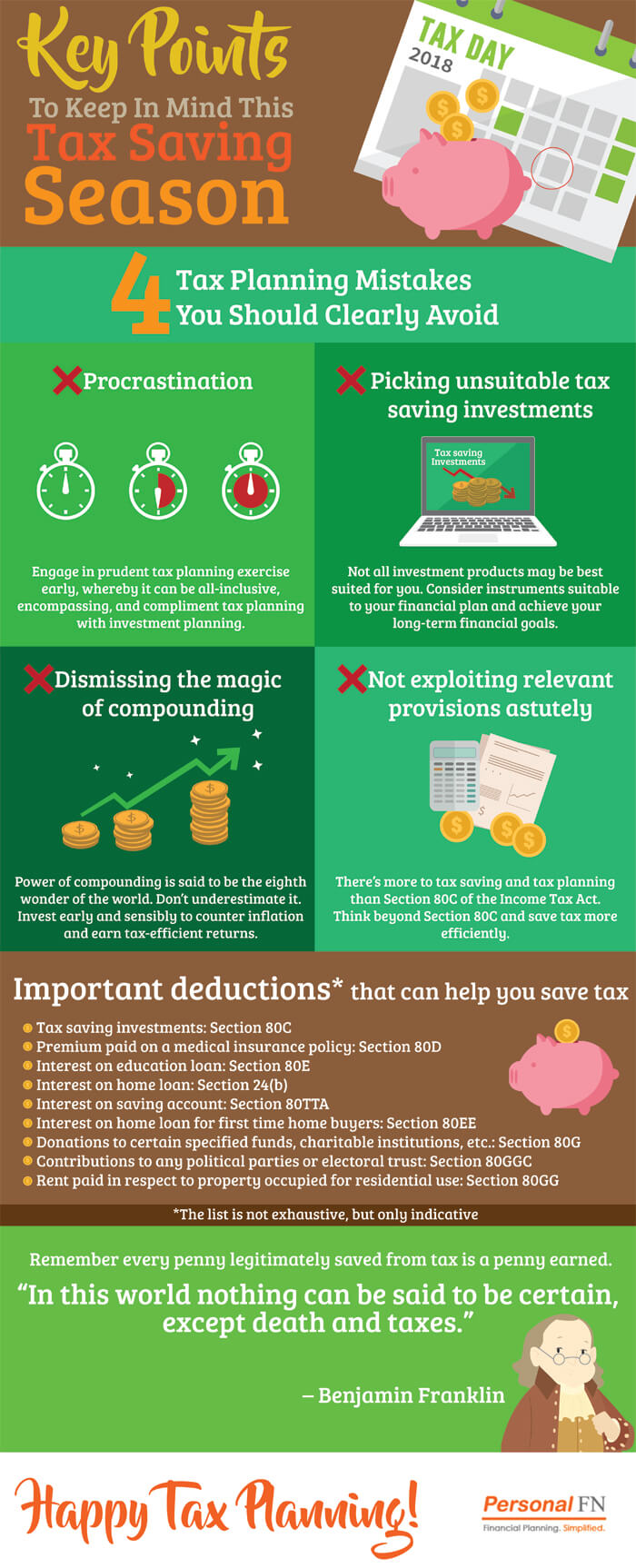

As Benjamin Franklin rightly said, “In this world nothing is certain but death and taxes”.

And being a law-abiding citizen, you are obliged to pay taxes on or before time each financial year.

Now paying tax is not a once-a-year, one-day activity. As you plan for all your goals in life, you need to plan for your tax payments as well.

Let us understand what is tax planning and the difference between tax planning and tax saving:

Tax planning is a holistic exercise

Tax planning is an exercise a tax payer does to meet tax obligations in a systematic manner by accounting for all payables, permissible exemptions, deductions, and reliefs available to you under the Tax Act.

With the financial year-end on the horizon, we feel the heat and realise, now is the time to make investments to save on tax. But have you ever wondered whether it is the prudent way for tax planning?

Unlike “tax saving”, which is generally done through investments in tax saving instruments/products, under “tax planning”, we take into consideration one’s larger financial plan after accounting for one’s age, financial goals, risk appetite, and investment horizon (including nearness to financial goals). By adapting to this method of “tax planning”, you not only ensure long-term wealth creation, but also protection of capital. Hence, please remember to commence your “tax planning” exercise well in advance and complement this with your overall investment planning exercise.

As you would know, tax is an obligatory payment made by citizens to the government. It is a fee charged by the government on a product, service, or income. Everyone aims to reduce their tax liability in order to protect their hard-earned money. Hence, tax saving activity is part of the whole tax planning exercise, whereby a tax payer can reduce his/her tax liability.

We recognise the fact that many of you are busy throughout the year, in your economic activities intended to make a living. But, if you have the same dedication in your tax planning exercise, the same will enable you to save more through tax planning and fulfil many of your dreams in life. Our experience reveals 4 mistakes that individuals make when saving taxes.

Mistakes to avoid while tax planning

- Procrastination

The root of all mistakes in tax planning — procrastination, which eventually leads to merely tax saving, rather than optimally planning for your taxes. And this, in return, is a sub-optimal way of exercising your rights as a tax-payer. Your haste often gets you to forget or ignore the facets of financial planning such as your age, income, ability to take risks and prioritising financial goals.

Remember, waiting till the eleventh hour is just going to lead you to a path of sub-optimal tax planning exercise, which defeats the true essence of a holistic tax plan.

- Unnecessarily buying insurance plans for the purpose of tax saving

As you near the end of the financial year, you receive calls and emails from insurance companies and agents urging you to buy an investment-cum-insurance plan — typically, market linked such as Unit Linked Insurance Plans (ULIPs) or some kind of Endowment plans. Realising the need to save your taxes, you may’ve even entertained these calls and eventually, doled a cheque to buy one. Have you introspected on whether you’ve done the right thing? Maybe not; either because you are uninformed or caught up in the urgency to save tax.

Remember when you think about insuring yourself, protecting your life against any unforeseen events; ideally, you must buy a pure term insurance plans, which gives due importance to your human life value. You may note that ULIPs are investment-cum-insurance plans where, for the premium paid, the insurance cover offered is peanuts compared to pure term life insurance plans. In the latter, for a lesser premium, you get a bigger life insurance cover. Precisely what is expected of a life insurance plan.

- Underestimating the power of compounding

The power of compounding is the most underrated facet of tax planning. Tax-payers and investors miss out on this earning due to procrastination and poor decisions while planning their tax outflows. To rise above inflation woes in the future, your current tax planning portfolio must include equity oriented mutual funds with a tax saving benefit. While most consider tax saving mutual funds, the ideal composition (based on risk appetite) is hardly achieved. This is another reason why tax-saving portfolios give sub-optimal returns.

We appreciate that some investors are risk averse. But if your age, income, and investment horizon permits you to take equity exposure, take a calculated leap of faith.

- Failing to optimise all available options for tax saving

For many, tax planning starts as well as ends with Section 80C of Income-tax Act, 1961. However, investing only in these investment instruments will not optimally reducing your tax liability. There are many other options available apart from Section 80C which you should look into. Thinking beyond 80C may help you save more for your other financial goals.

To bring to your notice, our Income Tax Act, 1961 also considers the humane side of our life and also gives deductions for contributions you make on such developments. So, in case if you pay your medical insurance premium, incur expenditure on the medical treatment of a “dependant” handicapped, donate to specified funds for specified causes, take a loan for pursuing higher education, or if you are an individual suffering from “specified” diseases; then all these expenses can help you effectively plan your tax obligations, optimally reducing your tax liability. Moreover, taking into account the urge to buy your dream home by taking a home loan can also extend tax saving benefits to you.

What are the tax-saving options under Section 80C?

Now, section 80C of the Income Tax Act enables an individual or a Hindu Undivided Family (HUF) to effectively invest in tax saving instruments, in order to optimally reduce their tax liability. This is seen as one of the most sought after sections when it comes to tax planning.

In order to leave more money in the hands of the salaried class, the deduction limit under this Section is currently at Rs 1.50 lakh p.a.

The Section offers you a host of popular investment instruments mentioned below, which qualifies for a deduction from your Gross Total Income (GTI):

- Life Insurance Premium

- Public Provident Fund (PPF)

- Employees’ Provident Fund (EPF )

- Sukanya Samriddhi Yojana

- National Saving Certificate (NSC), including accrued interest

- 5-Year fixed deposits with banks, Post Office, HUDCO

- Senior Citizens Savings Scheme (SCSS)

- National Pension System (NPS)

- Unit-Linked Insurance Plans (ULIPs)

- Equity Linked Savings Schemes (ELSS)

- Pension Plans

- Tuition fees paid for children’s education (maximum 2 children)

- Principal repayment on Housing Loan

Hence, if you invest in any or all of the aforementioned instruments; you would qualify for deduction under this section subject to the maximum of Rs 1.50 lakh p.a. But we think rather than just merely investing in any of the above tax saving instruments, you can also use these tax saving instruments for prudent tax planning.

(Read more for All You Need To Know About Section 80C )

Here is an awesome opportunity whereby you don't have to search for which ELSS mutual funds to invest in. Avail of PersonalFN’s Exclusive Report - 3 Tax-Saving Mutual Funds For 2018.

You will find the Top 3 ELSS that are geared to grow your investment multi-fold over long term while saving your taxes. These Top 3 ELSS are handpicked through our special 7-point Selection Matrix methodology, and are considered to be potentially the best tax-saving mutual funds in the Indian market.

What are the tax-saving options under Section 80D? The premium paid by an Individual or HUF on medical insurance policy to cover your family (including spouse and children) and parents against any unexpected medical expenses, qualifies for a deduction under Section 80D.

- Tax deduction on health insurance premium paid for you & your family

- Tax deduction on health insurance premium paid for your parents

- Tax deduction on preventive health check-up expenses

- Tax deduction on medical expenses of super senior citizens

The maximum deduction possible under this section is Rs 60,000. Below is the table will give you brief idea of deduction limits under section 80D:

| Individuals covered |

Exemption Limit |

Preventive Health Check-Up Expense |

Total |

| Self and family (self, spouse and dependent children) |

Rs 25,000 |

Rs 5,000 |

Rs 25,000 |

| Self & family + parents |

Rs 50,000 = Rs (25,000 + 25,000) |

Rs 5,000 |

Rs 55,000 |

| Self & family + senior citizen parents |

Rs 55,000 = Rs (25,000 + 30,000) |

Rs 5,000 |

Rs 60,000 |

| Senior citizen self & family + senior citizen parents |

Rs 60,000 = Rs (30,000 + 30,000) |

Rs 5,000 |

Rs 65,000 |

| Tax Slabs |

Tax rate |

Applicable Amount |

Balance |

Tax |

| 0- 250000 |

0% |

2,50,000 |

5,59,300 |

- |

| 250001 - 500000 |

10% |

2,50,000 |

3,09,300 |

25,000 |

| 500001 - 1000000 |

20% |

3,09,300 |

- |

61,860 |

| > 1000000 |

30% |

- |

- |

|

| Tax on Income |

86,860 |

| Education Cess @3% on Income tax payable |

2,606 |

| Total Tax Liability |

89,466 |

| Tax per Month |

7,455 |

In case you are non-senior citizen paying self, spouse, and dependent children, the maximum amount allowed annually as a deduction is Rs 25,000. And, if you are a Senior citizen paying health insurance premium for yourself, the maximum deduction is Rs 30,000

So, if you pay medical insurance premium for your parents (irrespective of whether they are dependent on you or not), you can claim an additional deduction of upto Rs 30,000 in case parents are senior citizens or Rs 25,000 in other cases under this section. So, for example, if you pay a premium of Rs 15,000 for yourself and Rs 20,000 for your parents, you will be eligible for a total deduction of Rs 35,000 only, assuming your parents are not senior citizens.

How a home loan can help save tax [Sec. 80C and Sec. 24(b)]

While all of us have a dream of buying a dream home or constructing or reconstructing or repairing our homes, it’s also important to consider the tax angle when we decide to do any of these activities. For some of us, the amount of wealth we have created allows buying or constructing or reconstructing or repairing or renewing homes from our own funds, i.e. without opting for a “home loan”. Then again, doing so precludes you to avail of the tax benefits attached if one takes a loan for such activities.

Yes, our Income Tax Act, 1961 too considers our desire to buy, construct, reconstruct, repair, or renew our dream home and is benevolent, as it provides you with tax benefits (that come along with it). Both, “repayment of principal amount” and “payment of interest” are eligible for tax benefit.

The “repayment of principal amount”, makes you eligible to claim a deduction upto a sum of Rs 1.50 lakh under Section 80C. This is available irrespective of whether you stay in the same property (Self Occupied Property - SOP), or have let it out on rent (Let Out Property - LOP).

In union budget 2016, the Government re-introduced Section 80EE (which was initially introduced effective 2013-14 and was applicable for only 2 assessment years, 2014-15 and 2015-16) for first time home buyer to avail an additional tax benefit of Rs 50,000, after satisfying certain conditions which are:

✔Value of the property is Rs 50 lakh or less

✔ Loan taken for this house is Rs 35 lakh or less

✔ Loan has been sanctioned by a financial institution or a housing finance company

✔ Loan has been sanctioned between 01-04-2016 and 31-03-2017

✔ As on the date of the sanction of the loan no other house is owned by you

But the additional tax benefit exemption can be availed after first exhausting limit under Section 24(b) for the interest portion.

The payment of interest amount (for the loan amount availed) is available for deduction under Section 24(b). In the first full budget of the Modi-led-NDA Government announced in July 2014, the deduction limit on interest payment of a home loan on a self-occupied property was increased from Rs 1.50 lakh to Rs 2.00 lakh. If you as “first time home buyer” a satisfy conditions as mentioned above for Section 80EE, the maximum sum you can avail for interest deduction under Section 24(b) is Rs 2.00 lakh for SOP, plus an additional tax benefit of Rs 50,000 under Section 80EE. But if the house purchased on a loan does not satisfy the conditions mentioned to enjoy additional tax benefit under Section 80EE, you can’t claim the additional benefit under Section 80EE.

In case of let out the property on rent (LOP), the actual interest payable is eligible for deduction under Section 24(b), thereby not being subject to any maximum limit. This applies even in the case where you have two home loans for two different properties, where one is self-occupied and the other is let out on rent.

Similarly, if you have taken a loan for the purpose of reconstructing, repairing, or renewing the property, the amount of deduction under Section 24(b) you are eligible for will be restricted to Rs 30,000, irrespective whether you want to stay in it or let it out on rent.

How education loan can help save tax [Sec. 80E]

While pursuing a personal goal of enrolling for “higher education” in order to be competitive enough to meet your financial goals; the Income Tax Act offers you deduction (from your Gross Total Income) on the interest paid, when you avail of a loan.

You can even take an education loan for your spouse or children’s or for any person (minor) for whom you are the legal guardian. But that makes you eligible for deduction under Section 80E of the Income Tax Act, to the extent of the interest paid on such a loan taken. It is noteworthy that HUFs are not allowed to claim deduction under section 80E in respect of interest paid on loan taken for higher education.

The deduction is available for a maximum of 8 years or till the interest is paid, whichever is earlier. So, to simplify it further, the deduction is available from the year you start paying the interest on the loan, and the seven immediately succeeding financial years or until the interest is paid in full, whichever is earlier.

Here the term “higher education” means full-time studies for any graduate or post-graduate course in engineering (including technology / architecture), medicine, management, or post-graduate courses in applied science or pure science including mathematics and statistics. But from the Finance Act of 2011, its scope has been extended to cover all fields of studies (including vocational studies) pursued after passing the Senior Secondary Examination or its equivalent from any school, board or university recognised by the Central or the State Government or local authority or any other authority authorised by the Central or the State Government or local authority to do so. However, no deduction is available for part-time courses.

It is vital to note that deduction can be claimed only if the loan has been taken from a bank, approved financial institution, or an approved charitable institution.

(Read more: Everything About Education Loan You Need To Know)

How helping a cause/donating can save tax [Sec. 80G]

As mentioned earlier, our Income Tax Act also considers the humane side of our life, and so if on humanitarian grounds you donate to certain specified funds, charitable institutions, approved educational institutions etc., the donation amount qualifies for deduction under this Section.

The deductions allowed can be 50% or 100% of the donation, subject to the limits stated under the provision of this Section. For example, donations to “National Defence Fund” set up by the Central Government are allowed 100% deduction, while for “Prime Minister Drought Relief Fund” are allowed at 50%. If you make donations to any of the host of notified funds and/or charitable institutions, you are eligible for deduction under Section 80G.

In order to claim deduction under this section, you are required to attach a proof of payment along with your return of income.

Don’t forget to claim deduction for savings bank interest u/s. 80TTA

This Section allows individuals and HUF to avail a deduction for interest earned on a savings account (with a bank, co-operative society and post office) to the extent actual interest or Rs 10,000, whichever is lower. Thus, the interest income earned from a saving account over Rs 10,000 will be subject to tax as per your tax slab. The benefit of this section cannot be applied on interest earned on a term deposits (also known as fixed deposits).

How to save tax on your salary?

Many salaried individuals, fail to look beyond Section 80C. The income declaration form covers certain sections of the Income-tax Act, 1961, but this is not the only route to save tax.

Let us look at Rohan’s case:

As a senior consultant with a multi-national company, Rohan earns a pay package of Rs 12 lakh per annum. His net taxable salary after all deductions, adds up to around Rs 6.70 lakh p.a. — this is after exhausting the limit of Rs 1.50 lakh available under Section 80C .

He feels helpless and cannot perceive other options amid a time when he has to file an investment declaration with the HR department of his organisation. As result, his current direct tax outgo works out to Rs 64,746.

It would be prudent to avail the benefits of the other Sections as well, so as to ultimately reduce the tax outgo. It's important to optimally restructure your salary!

But, before we explain how to restructure your salary to save on tax, let us first look at your current salary structure to understand how the components thereto influence the taxable income.

Rohan's employer offers him allowances: house rent allowance, leave travel allowance, conveyance allowance, and medical reimbursements. The total exemption limit available under these sub-headings works out to Rs 3.58 lakh. However, he is able to claim Rs 2.38 lakh. This, along with the investments of Rs 1.50 lakh under Section 80C, reduces his net taxable income to Rs 8.09 lakh. On this income, he has to pay tax of Rs 89,466 or Rs 7,455 per month. Here's the calculation in the table below:

| Tax Computation |

(in Rs) |

| Gross Salary |

12,00,000 |

| Salary Structure |

|

| Basic Pay |

6,00,000 |

| EPF Contribution @12% |

72,000 |

| House Rent Allowance |

3,00,000 |

| Leave Travel Allowance |

24,000 |

| Conveyance Allowance |

19,200 |

| Medical Reimbursement |

15,000 |

| Other Allowance |

1,69,800 |

| Exemptions Allowed |

|

| House Rent Allowance (Section 10 (13A)) |

1,80,000 |

| Leave Travel Allowance (Section 10 (5)) |

24,000 |

| Conveyance Allowance (Section 10(14)) |

19,200 |

| Medical Reimbursement (Section 17(2)) |

15,000 |

| Total Exemptions under Section 10 & 17 |

2,38,200 |

|

|

| Profession Tax |

2,500 |

|

|

| Deductions under sec 80C |

1,50,000 |

| Net taxable income* |

8,09,300 |

Note: *Assuming income from salary is the only source of income

The reason Rohan wasn’t able to avail complete exemption for the allowances was because the different components in his salary were not optimally structured. To understand the different components of the salary structure, read on …

Basic Salary: The basic pay forms the base component for other benefits such as provident fund, House Rent Allowance (HRA), etc. While a higher basic means higher benefits, on the flip side, it is fully taxable. Therefore, it is necessary to have an ‘optimal’ basic salary. A very high basic salary may result in a higher tax outgo.

HRA: If your residence is a rented one or paying-guest accommodation and your organisation provides you HRA benefits, it can lower your tax liability. Likewise, if you stay with your parents in an accommodation owned by them, you could pay them rent.

The maximum amount that can claimed as an exemption under HRA is the least of –

- Actual HRA; or

- Rent paid in excess of 10% of basic salary + Dearness Allowance (DA) if in terms of service; or

- 50% of basic salary + DA in case of Chennai, Delhi, Kolkata, Mumbai (40% of salary + DA in case of other cities)

Therefore, for Rohan to claim full HRA of Rs 3.00 lakh, he needs to pay a minimum rent of Rs 30,000 p.m. or Rs 3.6 lakh p.a. (Total rent paid is Rs 3.6 lakh; 10% of basic is Rs 60,000. Rent paid in excess of the basic salary is Rs 3.6 lakh minus Rs 60,000, which is Rs 3 lakh).

If Rohan stayed in a self-occupied house, he is not entitled to any HRA deduction and the entire HRA amount is taxable. If he had taken a loan to own this property, he could have claimed tax deductions on the home loan.

Unfortunately, Rohan pays Rs 20,000 p.m. as rent and is eligible for HRA, but cannot claim the full amount. Therefore, it would make sense for Rohan to reduce his basic and HRA. With the H.R. department, he can explore other allowances to balance out the gross salary.

Leave Travel Allowance (LTA) : As a salaried individual, you can claim LTA for any journey made either alone or with dependent family members in India. The maximum amount you can claim is the least of:

- The amount actually incurred; or

- The amount of LTA allowed

The exemption extended is for two journeys performed in a block of four calendar years. The current block is 2014-2017. It is vital to note that the exempted amount is restricted only to expense incurred on travelling to the destination and does not include expenses such as hotel bills, food, etc.

Transport allowance: Expenses incurred to commute between your home and work place is also exempt from tax. The maximum amount that is exempt is Rs 1,600 per month.

Medical reimbursement: Expenses incurred by you or your family for medical purposes can also help in reducing the tax liability. A maximum of Rs 15,000 can be claimed every financial year on account of medical expenses. But to claim this, you are required to submit, to your employer, the medical bills for the financial year stating the total amount you intend to claim.

Rohan has claimed all the exemptions that are allowed. So, what else can his employer include by which he can save tax? Well, here’s a list of it in the table below:

|

Exempt Salary Allowances |

|

| Allowance |

Exemption |

Maximum limit |

| Children Education Allowance |

Rs 100 per month per child up to a maximum of two children |

Rs 2,400 p.a. for two children |

| Children Hostel Expenditure |

Rs 300 per month per child up to a maximum of two children |

Rs 7,200 p.a. for two children |

| Conveyance Allowance |

Allowance granted to meet the expenditure on conveyance in performance of duties of an office |

Exempt to the extent of

expenditure incurred |

| Research Allowance |

Expenditure incurred for encouraging the academic research and other professional pursuits |

Exempt to the extent of

expenditure incurred |

| Meal Vouchers |

Food in office premises or through non-transferable paid vouchers usable only at eating joints provided by an employer is not taxable, if cost to the employer is Rs 50 (or less) per meal |

Depends on the number of working days. If a company works 25 days a month, the amount will work out to Rs 2,500 p.m. (Rs 50*2 meals *25 days) or Rs 25,000 p.a. |

| Gift Voucher |

Gifts in cash or convertible into money are fully taxable |

Rs 5,000 p.a. |

|

b) Gift in kind or vouchers up to Rs.5,000 in aggregate per annum would be exempt, beyond which it would be taxable. |

|

| Mobile/telephone reimbursement |

Expenses on telephones including a mobile phone incurred by the employer on behalf of employee shall not be treated as taxable perquisite. |

Exempt to the extent of expenditure incurred |

| Newspaper and periodicals |

Subscription or purchase of newspapers, books and periodicals relating to your profession are fully exempt against actual bills |

Exempt to the extent of expenditure incurred |

| Motor Car Allowance |

The maintenance and running expenses are fully exempt under certain conditions for a car owned by the employer or employee. |

Out of the total expenses, only a very small portion may get taxed subject to certain conditions |

Here's how Rohan can restructure his salary to reduce his tax outflow…

First, reduce the basic pay to Rs 4.8 lakh. Thus, his HRA will fall to Rs 2.4 lakh and can be claimed to the full extent. The only concern is that his contribution to EPF will fall as well, reducing the amount eligible under Section 80C. However, he's not worried as he contributes Rs1 lakh to tax-saving equity mutual funds.

Rohan can get his employer to include other allowances in his salary structure, through which he can claim exemption. By doing this, he can claim an additional of Rs 36,000 as exempt income through meal vouchers and other allowances. With a higher amount claimed under HRA, his total taxable income falls by as much as Rs 56,000.

Thus, Rohan's tax outgo will be reduced by nearly Rs 12,000 to Rs 77,930 or Rs 6,494 p.m. A lower PF contribution, thanks to a lower basic pay, can take his net in hand salary up by Rs 35,536 p.a. Take a look at the table below…

| Tax Computation |

Current (Rs) |

Restructured (Rs) |

| Gross Salary |

1,200,000 |

1,200,000 |

| Salary Structure |

|

|

| Basic Pay |

6,00,000 |

400,000 |

| EPF Contribution @12% |

72,000 |

48,000 |

| House Rent Allowance |

3,00,000 |

200,000 |

| Leave Travel Allowance |

24,000 |

24,000 |

| Conveyance Allowance |

19,200 |

19,200 |

| Medical Reimbursement |

15,000 |

15,000 |

| Other Allowance |

1,69,800 |

493,800 |

| Exemptions Allowed |

|

|

| House Rent Allowance (Section 10 (13A)) |

1,80,000 |

200,000 |

| Leave Travel Allowance (Section 10 (5)) |

24,000 |

24,000 |

| Conveyance Allowance (Section 10(14)) |

19,200 |

19,200 |

| Medical Reimbursement (Section 17(2)) |

15,000 |

15,000 |

| Other exempt allowance |

|

|

| Total Exemptions under Section 10 & 17 |

238,200 |

294,200 |

|

|

|

| Profession Tax |

2,500 |

2,500 |

| Income chargeable under head 'Salary' |

959,300 |

903,300 |

| Deductions under sec 80C |

150,000 |

150,000 |

| Net taxable income* |

|

|

| Tax on Income |

86,860 |

75,660 |

| Education Cess @3% on Income tax payable |

2,606 |

2,270 |

| Total Tax Liability |

89,466 |

77,930 |

| Tax per Month |

7,455 |

6,494 |

Note: *Assuming income from salary is the only source of income

So, Rohan can effectively reduce his taxable income just by restructuring his salary.

But this restructuring is specific to his profile. You need to restructure your salary to suit your needs and expenses. For example, if your job requires you to travel a lot, you can ask them to include a higher conveyance allowance. There's a whole list of other allowances you can consider exploring here.

Apart from exempt allowances, Section 80C; you need to look at all other deductions under chapter VIA of the Income-tax Act, 1961. If you are not receiving any HRA, you can get a deduction on rent expenses under Section 80GG. Or, you can get a deduction on incurred expenses in treatment of a dependent member of your family under Section 80DD. Like these, there are several under sections under which you can claim deduction for specific expenses.

To conclude…

Last minute tax planning can lead to lower savings and inefficient investments. PersonalFN is of the view that you need to plan your taxes at the start of the year, to see where you stand and make adjustments accordingly. It is important for you to know the various routes to save tax on your income the legal way. To get started, download our latest tax planning guide here. It will help you crosscheck whether you are on the right track to saving and planning your taxes and to take timely action before you miss out on any benefits.

You can also access Personalfn EPF calculator here.

Add Comments