| S&P BSE Sensex* |

Re/US $ |

Gold Rs/10g |

Crude ($/barrel) |

FD Rates (1-Yr) |

32,832.94 |-846.30

-2.51% |

64.46 |0.11

0.17% |

29,250 | -235.00

-0.80% |

62.48 |-0.74

-1.17% |

5.0% - 6.75% |

Weekly changes as on November 30,

2017 BSE Sensex value as on December 01, 2017

Impact

“With great power, comes greater responsibility!”

And, what happens when a person rises in power?

People begin look up to them as leaders in their field.

What happens when a leader proves their mettle?

They start to receive greater acceptance and responsibility.

Their circle of influence extends further.

The same is true with currencies.

As the popularity of a currency goes up and its user-base expands, the value of a currency goes up.

No wonder Bitcoin is buzzing these days…

(Image source: freeimages.com)

You might be surprised to know that the value of one Bitcoin recently touched US$ 11,000 — a ten-fold jump in one year. However, what goes up, must come down. And soon after claiming a life-time high, the Bitcoin prices fell a massive 20% during the same trading session.

Such inexplicable swings create as much anxiety than excitement.

Investors in the Bitcoin are on cloud nine. But sceptics who missed out, claiming it was a bubble, have now labelled it a fraud.

In the global arena, many people are in a state of confusion — they aren’t fully informed about precisely what the Bitcoin is. On the other hand, they don’t want to miss the bus if it is indeed “gold” of the future.

If you are one of them, this is the right article to read.

Bitcoin currently is the largest circulated and perhaps, the most famous cryptocurrency.

In layman terms, cryptocurrencies are alternative and unregulated digital currencies held as assets and exchanged for real goods and services as well.

Let’s first understand why Bitcoin, or any other cryptocurrency for that matter, exists.

As you know, the conventional monetary system has many flaws. Transfer of money from one person to another is subject to the involvement of multiple institutions including the banks of both parties, their ATM networks, red-tape, governing authorities, financial policies of their countries, and so on.

Such a multi-layer system not only adds to costs, but also leaves a massive room for human and technical errors associated with the transaction. Plus, the survival of a currency vastly depends on the credibility of the government of a nation issuing it. When the governments are toppled or countries go bankrupt or crumble under the foreign debt-pile or go to war; domestic currencies of such countries go for a toss.

Proponents of cryptocurrencies claim that digital currencies are free from any government or central bank intervention. They are an improved version of the conventional monetary system. To facilitate the transactions between peers, i.e. between people who want to trade among themselves, cryptocurrencies use complex mathematical operations instead of involving mediators such as banks.

Emerging technologies make cryptocurrencies safe and decentralised. You might be astonished to know, cryptocurrencies including Bitcoin need to be excavated — just like gold. The only difference is unlike human labours, Bitcoin miners are technology experts who can solve complex mathematical problems and mine a Bitcoin. They also ensure security and the smooth functioning of the network.

The total minable Bitcoins are 21 million. Out of which 16.7 million have already been mined. The last Bitcoin may be extracted in 2140. Just as in case of gold, once the shallow deposits are excavated, you need to dig deeper. This is where Bitcoin mining gets difficult as more miners try their luck.

Investors believe as the new Bitcoins are hard to mine; the value of the existing stock shall skyrocket in coming years. Self-proclaimed cryptocurrency experts predict, Bitcoin is set to zoom past the US$ 1 million mark per piece over next 5-10 years.

Taking a serious note of the investors’ frenzy, Nasdaq Exchange in the U.S. has planned to launch Bitcoin future series in the first half of 2018. However, this can lead to a dramatic increase in the speculation about the future value of the virtual currency. Once the large-scale short-selling—selling without possessing an asset—becomes possible, Bitcoin may turn more into a speculative asset than currency. From a transactional perspective, acceptance of Bitcoin is minimal; but everybody investing in it is convinced about the future.

There’re over 1,000 cryptocurrencies on offer. Each claims to hold a promising future. A camp that considers cryptocurrencies are a scam, firmly believes most of them won’t exist after a few years.

At the other end of the spectrum, you have investors betting big on the cryptocurrencies, including Bitcoin. While on the other, there’re central banks, governments, and other social-political establishments that are cautious to welcome the virtual currencies; primarily because they are finding it challenging to shun cryptocurrencies straight off given their popularity.

At present, several questions are being raised about the legitimacy and transparency of cryptocurrencies. It still remains to be seen how far they go and which ones survive.

Right now, the market cap of Bitcoin is higher than that of companies such as IBM and Disney. In other words, the value of already mined Bitcoin is abysmally low, since it can buy you not more than a few listed companies. Thus, it’s far from establishing itself as a genuine alternative to fiat currencies. Does that mean the value of Bitcoin will rise so much that it will soon become liquid enough to support the existing financial system?

Well, the answers will be known only in the future. With the cross-border movement of financial assets becoming increasingly difficult — thanks to rigorous compliance practices adopted by various nations, the medium of exchange that recognises no boundaries seems to have become the need of the hour.

Is it merely a coincidence that value of Bitcoin rose after the U.S. government launched an attack on the unaccounted wealth of U.S. citizens stashed in other countries? Too good to be true. According to Deutsche Bank, estimates of the total value of global financial assets were around US$ 300 trillion in 2014. If even 1% those assets flow into Bitcoin, in search of safety, the case may look more convincing.

Still, when you look at the journey of Bitcoin so far, which has a history of less than a decade, it seems enigmatic and resembles historical infamous investment bubbles.

Now the difficult question…

Should you invest in Bitcoins?

PersonalFN is of the view that, given the findings by RBI and observations of the Supreme Court on virtual currencies and it raising a red flag, thereto, it would be best to avoid using Bitcoins to make e-payments or indulge in them even in the form of trading. Although it may enable you to transact at high speed and at a low cost. This is because virtual currencies are unauthorised by any central banks or monetary authority. They don’t have a clear legal status, and the chance of misuse of e-wallet is high (through various ways); could result in an unintentional breach of anti-money laundering or combating the financing of terrorism laws, which can subject one to prosecution.

Want to know how to strategically multiply wealth over next 7-8 years? Try PersonalFN’s “The Strategic Funds Portfolio for 2025” based on the core and satellite approach to investing.

Here are 6 benefits of ‘core and satellite approach’:

- Facilitates optimal diversification;

- Reduces the risk to your portfolio;

- Enables you to benefit from a variety of investment strategies;

- Aims to create wealth cushioning the downside;

- Offers the potential to outperform the market; and

- Reduces the need for constant churning of your entire portfolio

‘Core and satellite’ investing is a time-tested strategic way to structure and/or restructure your investment portfolio.

Your ‘core portfolio’ will consist of large-cap, multi-cap, and value style funds, while the ‘satellite portfolio’ will include funds from the mid-and-small cap category and opportunities style funds.

And that’s not all. You will also master the art of astutely structuring the portfolio by assigning weightages to each category of mutual funds and the schemes you select for the portfolio. PersonalFN’s “The Strategic Funds Portfolio for 2025” is geared to potentially multiply your wealth in the years to come. Subscribe now!

A Month To Go, Have You Linked Your Aadhaar?

Impact

The deadline to link your Aadhaar to various documents and services is fast approaching.

As of now, December 31, 2017 is the last date to link Aadhaar to your bank account, mutual fund folios, demat account, and insurance policies.

There may be an extension in date, given that this matter is still in court, do not bank on it.

The Supreme Court is yet to set up a Constitution bench to hear the issue of stay against mandatory linking of Aadhaar with bank accounts, mobile phone numbers etc. The apex court said it will hear a batch of petitions challenging the mandatory linking of Aadhaar to important services in the first week of December.

Earlier this week, the Government informed the apex court that it is willing to extend the deadline to March 31, 2018. However, as per reports, that the deadline may be pushed back for only those who do not have an Aadhaar. Hence, for those who do, the existing deadline will remain in force.

Given that the government is hell bent on using this Unique Identification Document (UID) to remove duplication and curb illicit money, you may soon have to link Aadhaar to important services if you wish to continue using them.

This requirement has been brought into the law via the Prevention of Money-laundering (Maintenance of Records) (Second Amendment) Rules, 2017, which have been notified by the government under powers delegated to it by the parliament through the Prevention of Money Laundering Act, 2002.

While it remains to be seen how the Supreme Court assesses the issues associated with Aadhaar linkage, until then, it is wise to comply with the government’s directive and link Aadhaar number to your different accounts to avoid it being frozen.

PersonalFN has put together the list of important documents and services to link your Aadhaar in a few simple steps.

To read more and know the steps to link Aadhaar, please click here.

Filing Revised I-T Returns? Make Sure You Don’t Misuse It

Impact

If you have filed a revised tax return post demonetisation, Income-Tax (I-T) Department is likely to put you under a microscope soon. The Central Board of Direct Taxes (CBDT) has advised the taxman to take strict action against assessees who have misused the facility of filing revised returns to turn black money into white merely by declaring it as income.

As you may be aware, many hoarders of cash blindly deposited demonetised currency in their bank accounts hoping to get away with it. To make their position slightly more concrete, they filed revised tax return for the Financial Year (FY) 2016-17. CBDT has advised Assessing Officers (AOs) to scrutinise all such cases and charge heavy penalties if they discover any attempt of turning black money into accounted income.

Formal instruction of CBDT read as follows: “Unaccounted income so assessed in scrutiny assessment is liable to be taxed at a higher rate without any set off losses, expenses etc. under section 115BBE (treatment of tax credits) of the I-T Act."

Professionals and business persons who have reported higher income by way of higher sales in the revised return filed (post demonetisation) will be grilled to find out the source of income. A CBDT directive in this regard says, "The source of cash in hands of the person who had made payments to the assessee has to be verified carefully and the past profile of the assessee concerned should be thoroughly analysed."

Commenting more about these developments a senior tax official said, "The assessing officers will comply with these new directions or guidelines in conducting over 20,000 cases of scrutiny, already selected by the department based on their financial activity post note ban."

To read the diffference between Income Tax Rectification request and Revised Return , please click here.

How You Should Structure Your Debt Fund Portfolio

Impact

In a falling interest rates environment yields drop and bond prices rise. Debt fund investors enjoy double-digit returns in such interest rate phases.

Exactly this happened between April 2014 and December 2016, when the Reserve Bank of India (RBI) reduced rates by 175 basis point to 6.25% from 8%. It was one of the best periods for long-term debt funds over the past decade.

With the decline in bond yields, long-term debt funds or income funds generated returns in excess of 12% compounded. Over 65 schemes delivered double-digit returns. The set of over 150 debt schemes generated an average return of 10%.

Given the massive returns over this period, do you feel debt funds are safe?

To Personal FN’s views and strategy, please click here.

Best Balanced Funds In 2017: Should You Invest?

Impact

As the market scales to new highs, investors become wary. During such times, distributors, advisors, and at times even mutual fund houses aggressively push balanced mutual fund schemes.

And investors are encouraged to seek out the best balanced mutual funds.

Unfortunately, when it comes to pick the best mutual fund schemes, investors tend to give a high weightage to recent performance and star ratings. This is why schemes with the best returns over the past 1-year or 3-year periods tend to gain the maximum inflows from investors.

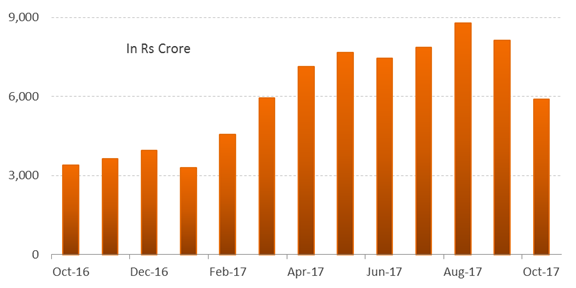

Net Inflows in Balanced Funds In the Past One Year

Data as on October 31, 2017

(Source: ACE MF, PersonalFN Research)

Over the past one year, the net inflows into balanced mutual fund schemes have more than doubled. From around Rs 3,000 crore a year ago, the net inflow nearly tripled to Rs 9,000 crore in August 2017, before moderating to about Rs 6,000 crore in October 2017. In March 2017, net inflows into balanced funds even outpaced equity diversified funds. Clearly, investor participation has grown multi-fold.

To read about the best performing balanced funds and Personal FN’s view, please click here.

Now Get A Share Of Your PF Contribution In ETF Units

Impact

The Employees’ Provident Fund——a publicly managed old-age income security scheme——invests upto 15% of its corpus in equities. However, currently, the benefits of equity investments neither get reflected in the interest rate calculation nor in the subscriber’s account?

Before you make a bee line to protest, the good news is that this scenario is going to change soon.

What is the reason?

Employees’ Provident Fund Organisation (EPFO) has recently modified its accounting policy. As a result of this, EPF subscribers will get to see the credit of Exchange Traded Fund (ETF)units to their account. EPF passively invests in equity markets through the ETF route.

Right after the EPFO announced this decision, Ms M. Sathiavathy— Labour Ministry secretary—said to the media, “EPFO has invested around Rs. 32,000 crore so far in the ETFs. The return on investment so far is 21.87 per cent. But this is notional because the EPFO would get this return only when it would liquidate this investment.”

To read more about this story and Personal FN’s views over it, please click here.

And Other News...

India’s Gross Domestic Product (GDP) quickened at 6.3% in Q2, FY 2017-18, i.e. in the July-September quarter of the current fiscal. Mining and manufacturing industries performed well and recorded 5.5% and 7.0% growth, respectively. Electricity demand grew steadily, hinting at a possibility of a sustained upturn in manufacturing. However, decline in agricultural growth and slower growth in public spending are the causes of concern. Unless agricultural activities gather momentum, the economy is exposed to a risk of inflation led by rising food prices. To sum up, the negative impact of demonetisation and the implementation of GST is proving to be transient indeed, as expected, but runaway growth still looks a distant dream.

Tutorials…

All You Need to know about Senior Citizen Savings Scheme (SCSS)

When Is The Best Time To Sell Your Mutual Fund?

NFO Review

BOI AXA Midcap Tax Fund - Series 1: Should You Invest?

Financial Terms. Simplified.

Fiat Money: Fiat money is currency that a government has declared to be legal tender, but it is not backed by a physical commodity. The value of fiat money is derived from the relationship between supply and demand rather than the value of the material that the money is made of. Historically, most currencies were based on physical commodities such as gold or silver, but fiat money is based solely on the faith and credit of the economy.

(Source: Investopedia)

Quote: “Price is what you pay. Value is what you get."-Warren Buffett,