To have that peaceful retirement most of us dream of, savings and planning must go hand-in-hand. There are a myriad of avenues you could undertake to plan your retirement prudently. One such investment avenue is National Pension Scheme (NPS) (add this sentence)

Earlier, the NPS was available only to Government employees, and since May 1, 2009 was introduced to citizens in the unorganised (private) sector. Clearly, the need for higher participation in pension contribution (through this product) was noticed.

The “National Pension System is offered by the

Pension Fund Regulatory and Development Authority (PFRDA).

So, any employee whether, employed in private sector, self-employed, or professional can enjoy the pension benefits under NPS.

Many opt for the NPS with the point of view of

tax planning , or owing to a dearth of other retirement products available.

However, this is due to a lack of awareness. Many investors lack an in-depth understanding about the product. Let’s look at the deterring factors of the NPS:

- Inefficient Taxation:

NPS does not enjoy the Exempt-Exempt-Exempt (EEE) status, unlike Employees Provident Fund (EPF) and Public Provident Fund (PPF). As per the current tax laws, 60% of the accumulated retirement corpus will be brought under the tax ambit, making it unpopular vis-à-vis PPF.

Moreover, the life annuity is mandatory for a subscriber to purchase from the retirement corpus. Infact this is taxable as per the prevailing tax laws.

- Inability to beat inflation:

A subscriber to the NPS is forced to buy a life annuity from a life insurance company. Annuities offer paltry returns (in the range of 3% to 7% pre-tax) making it an incompetent instrument to beat inflation.

- Complex product:

The NPS is a complex product offering many types and options. At times, investors are overwhelmed with these options and the chance of opting for an incorrect account is high.

NPS offers an applicant the freedom to decide how his money will be invested. It offers two options—Active Choice and Auto Choice

Under the Active Choice, the entire pension wealth can be invested in Asset Class C (Corporate debt) or G (Government securities) and up to a maximum of 50% in Equity (i.e. Asset Class E).

In Auto Choice (i.e. Lifecycle Fund), the fraction of funds invested across three asset classes will be determined by a pre-defined portfolio. This option is good for investors lacking knowledge to manage their NPS investment.

(Source: PersonalFN Research)

Besides there's Tier-I and Tier-II account.

Tier I Account: It is a non-withdrawal account. This means withdrawals of the contributions one has made are not permitted.

Tier II Account: This account is a voluntary savings account. To have Tier-II account, you first need to have a Tier-I account.

The Tier-II account can be opened with a minimum contribution is Rs 1,000. In August last year, the regulator waived off the criteria of minimum contribution of Rs 250 as well as the minimum balance of Rs 2,000 at the end of the financial year.

From the Tier-II account, you are permitted to withdraw as and when you wish to. So, it operates like your saving bank account. However, since this account does not have a lock-in period for funds to be invested, a tax benefit is not applicable. Even if you hold both the accounts under the NPS, only the Tier-I account will be eligible for tax benefits.

(For more details read this article: Why NPS Is A Bad Investment For Your Retirement. )

- Long Lock-in period:

The NPS has a high lock-in period as the retirement age is fixed at 60 years. Therefore, you cannot withdraw completely from before you attain this retirement age. Unlike NPS, other retirement savings instruments, such as PPF, EPF, and Mutual Funds, do not have a lock-in period for more than 15 years.

Your PPF contributions are locked-in for 15 years and your money invested in ELSS funds can be en-cashed after completing 3 years.

- Pre-mature withdrawal:

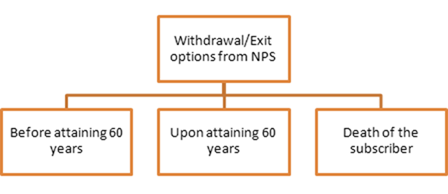

NPS offers 3 options for a subscriber to exit/withdraw the corpus as explained below:

(Source: PersonalFN Research)

- Before attaining 60 years:

To exit from the NPS before the age of 60, you need to be purchase a compulsory annuity of minimum 80% of fund value. The remaining 20% of the money can be withdrawn. But if the corpus is less than Rs 1 lakh, complete withdrawal is permitted.

- Upon attaining 60 years:

At the age of 60, you can exit the NPS. However, you are required to invest a minimum of 40% of the fund value to purchase a life annuity. And 60%, the remainder of the money, can be withdrawn in a lump sum or in a phased manner upto your age of 70 years. As per current tax laws, 40% of the money withdrawn on maturity is taxable. However, if the corpus is less than Rs 2 lakh, a withdrawal of the full amount is permitted.

- Death of the subscriber:

At the time of death of the subscriber, the entire accumulated corpus (i.e. 100%) will be paid to the nominee or legal heir. There will not be any purchase of annuity and the entire proceeds received will be tax-free in the hands of the nominee/legal heir.

To Sum-up…

PersonalFN is of the view that, NPS is ineffective to create a substantial corpus that will meet your retirement needs. It would work rather well, if you chalk-out a prudent financial plan with the help of a financial planner.

You can even use our

Retirement Calculator to estimate your expected retirement corpus.

Wisely invest as per the plan laid out (which would mostly recommend you equity allocation at younger age, and then as your age progresses balance the asset allocation between equity and debt instruments). You will be able to generate the substantial enough corpus to meet your retirements needs. Also under this scheme, when one withdraws money, at the age of 60, it is taxable. Thus, although the structure looks attractive on the face of it, the NPS falters in its goal of attracting more investors, although it provides a deduction under the Income Tax Act, 1961.

Moreover, under the present scheme, it is mandatory to purchase an annuity on retirement.

An annuity generates paltry returns, it isn't competent to beat inflation, and is taxable

If investing in the NPS appeals to you, make sure you aren't completely dependent on it. A judicious asset allocation is required to earn the maximum returns during your life’s golden years. Hence, consider other wealth creating investment avenues that can help you

plan your retirement well.

If you wish to have a professional guidance, do contact our

Certified Financial Guardian who will handhold you and guide you in every financial decision you make .

(You may also like to read:

Can NPS And PPF Help You Retire Comfortably?)

Add Comments

| Comments |

drsprakashmsorth@gmail.com

Dec 12, 2018

Up to what age can one invest and when can withdraw |

1