You have probably come to realise that regular plans of mutual fund schemes work out to be a costly affair for long-term investments.

If you invested in mutual funds before January 2013, the only plan option available was regular plans. Effective January 1, 2013, each mutual fund scheme that was available for subscription offered direct plans with a lower fees or expense ratio.

Direct plans, as the name suggests, are for direct investors who skip the intermediary or distributor. Due to which, these plans exclude distributor commissions, hence, are available at a lower fee to investors.

The difference in costs may seem like a few percentage points, but over the long-term, it could work out to lakhs of rupees.

To know more about the benefits of direct plans, do read: Mutual Fund Direct Plans - Everything You Need To Know

Over the past five years, many investors who realised the benefits may have already made the shift to direct plans.

Others may have inadvertently continued investing in regular plans through Systematic Investment Plans (SIPs) or have remained in the dark on this key regulatory change. Exit loads or even lock-in periods have dissuaded investors to switch from mutual fund regular plans to direct plans.

You may have invested in a regular plan on the advice of a distributor, but now as you no longer avail of their services, it will probably be wise to switch to direct plans.

However, before making the switch do remember, you need to be financial savvy to make prudent investment decisions. If you lack the expertise, don't worry, you can always avail of the services of a fee-based investment adviser.

Also read: Penny Wise & Pound Foolish? Here's Why Direct Plans and Trustworthy Advice Must Go Hand-in-Hand

But you need a financial planner or investment adviser who is a mark of trust and respect. They should exemplify the highest fiduciary standards at all times — handles your hard-earned money with enough care and prudence, much as how they would manage their own personal finances – with an unbiased and an independent approach. The recommendations need to be backed by rationale and scientific study.

A fee, however, is the monetary price you would have to pay to avail such a service.

Do have a look at PersonalFN's Comprehensive Financial Planning Service here.

Important factors to consider before switching from regular plans to direct plans:

(Source: pexels.com)

- Voids distributor services

As highlighted earlier, a switch from regular plans to direct plans will devoid you of the services of a distributor. If you need someone to handle the paperwork or facilitate transactions, several online platforms that are registered as investment advisers help you do this at a small fee. The fee could be in the form of per transaction cost or a monthly or annual subscription. Some provide additional services such as goal-based planning and top mutual fund recommendations. Do review all platforms and avail of a service that provides trustworthy and unbiased advice.

Do read: Does Your Robo-Advisor Provide Research-Backed Recommendations?

- Exit loads

When switching from regular plans to direct plans, the exit load criterion is applicable. Therefore, if the scheme charges an exit load of 1% from redemption of units held for less than a year, you will need to pay this charge on such units.

If you are investing in a regular plan via a SIP, the exit load period is calculated from the date of each monthly instalment. Hence, you may need to make the switches in tranches over a period to escape the exit load penalty.

Also remember, when you switch to the direct plan, it is considered as a new purchase. Hence, the new exit load tenure will begin from the date of the investment in the direct plan. Do keep this in mind if you have goals that are due to mature over the short-term.

- Lock-in periods

Equity Linked Savings Schemes (ELSSs), Retirement Funds, Children's Fund, or similar investments come with a lock-in period of 3-5 years. This means, you cannot redeem or switch the units before the expiration date of the agreed tenure.

Thus, before you plan to switch out of a regular plan to a direct plan, do make sure your units are free from a lock-in period. As in case of the exit load criteria, for investments via a SIP, the lock-in period is calculated from the date of each instalment.

Here again, when you switch to the direct plan, the lock-in period will start over on the investment. If you have goals that are due to mature within the next 3-5 years, a switch from regular to direct plans should be avoided.

- Tax implications

Yes, now here's another important factor to consider. Earlier, for equity mutual fund units held for greater than one year, long term capital gains (LTCGs) was tax-free. From FY2018-19 onwards, LTCGs of above Rs 1 lakh will attract a tax @10%.

So, if you have a sizable corpus in a regular plan, you may need to stagger your withdrawals over multiple years to avoid losing a large chunk of your money in tax.

Similarly, gains on debt funds too, attract tax. However, on LTCGs you get the benefit of indexation. Therefore, do weigh the costs and benefits of switching to a direct plan. As in the case of the exit loads and lock-in periods, the tenure to qualify for LTCG or STCG will start over from the date of investment in the direct plan. Do keep this in mind to avoid unnecessary tax outflows due to STCG tax implications.

- Investments made via a broker in demat form

If you have made investments via your stock broker, a direct switch to direct plans will not be possible as in other cases. This is because stock broking firms act as distributors, hence, provide only the regular plan option. In such cases, you may need to redeem your investments from your stock broker and reinvest through a direct mutual fund platform. You can also make the switch online or offline directly by approaching the fund house.

How to switch from regular plans to direct plans

(Source: pexels.com)

You've considered all the costs and tax implications and have decided to make the switch, here's how to do it -

Offline mode – 5 simple steps to switch from regular plans to direct plans

-

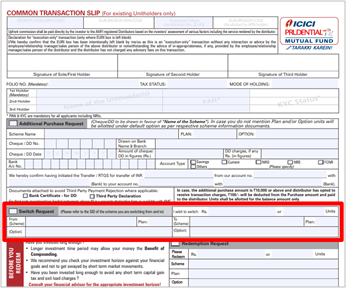

Visit the office of the fund house or the respective Registrar and Transfer Agent (RTA). You can locate the mutual fund office in your city here - https://www.amfiindia.com/investor-corner/. If you have MF Utility account, you may visit their service centres as well - https://www.amfiindia.com/investor-corner/online-center/locate-MFU.html

(Source: ICICI Prudential Mutual Fund, PersonalFN Research)

-

Ask for the Common Transaction Slip for purchase, redemption, or switch. You may download the form from the RTA or the AMC website. Pre-fill the form to ease the process at the AMC office or RTA. MFU transaction forms can be downloaded here - https://www.mfuindia.com/CTF. You can even prefill the form before printing.

-

Ensure all the details are correct, specifically the source scheme name and target scheme name, as well as the amount or number of units that need to be switched. Once verified, then Sign and Submit the form.

-

Collect the time-stamped acknowledgement as proof of submission.

-

As soon as the transaction is processed, you will receive details on your registered mobile number or email id.

Online mode – Switch from regular plans to direct plans in 5 convenient steps

-

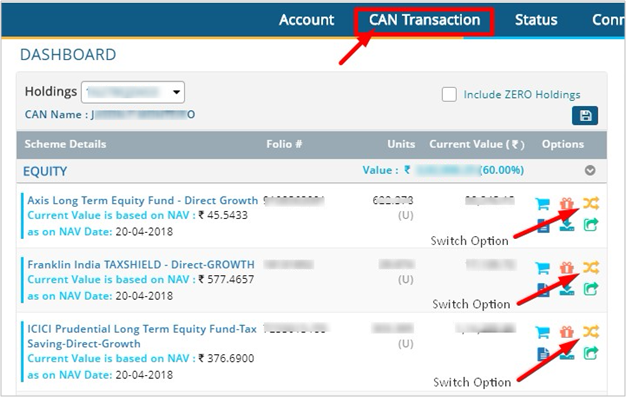

If you have registered for online access through the website of the AMC or RTA or MF Utility, you may conveniently submit the switch transaction request. Once registered, login to access or view the fund holdings.

(Source: MF Utility, PersonalFN Research)

- Some websites list the schemes with an option for additional purchase, redemption or switch request alongside. You can click on the switch icon to access the switch transaction page. All you need to do is input the amount or number of units to be switched, and the source scheme name and then submit..

If there isn’t an option to switch besides the scheme name, proceed to the transaction page and choose the Switch option. Here you will need to pick the Source scheme from your list of holdings and the Target scheme. Enter the amount or number of units and proceed.

-

A confirmation page will be displayed with a summary of the transaction. Ensure all details are correct and that the target scheme is correctly chosen. Proceed by giving your confirmation.

-

Certain portals may require a transaction PIN or ask you to re-enter your login password as an added security measure. Provide the authorisation to complete the transaction.

-

On successful completion of the Switch, you will receive a confirmation on your registered mobile or email id.

As seen above, the process is fairly simple to switch from a regular plan to direct plan. However, before switching, it is pertinent to foresee the implications of such a transaction. You need to evaluate the impact it will have on your financial goals.

However, for fresh investments towards long-term financial goals, do approach a fee-based investment adviser and invest in direct plans. You will end up with a huge savings over time.

If you require some handholding on the path to wealth creation, to create a customised investment portfolio, or need to organise a financial plan in place, seek guidance from our Financial Guardian who can assist you in an unbiased and objective manner. Schedule a call here.

At PersonalFN, we put your interest before our own and recommend Direct Plans of mutual funds, adopting high fiduciary standards.

|

Editor’s note:

There’re thousands of mutual fund schemes on offer, and busy investors like you hardly get time to evaluate all of them before shortlisting a few.

Don’t worry! You still have a chance to invest in some of the most reliable schemes available in the market at present, without doing even an iota of work at your end.

You can rely on PersonalFN’s unbiased mutual fund reports.

As a part of its premium mutual fund research service, PersonalFN brings to you ‘FundSelect’—a research report which offers honest and unbiased mutual fund recommendations. Along with clear recommendations, FundSelect also summarises reasons to buy/hold or sell a scheme in a crisp form.

For serious readers, it renders a comparative study with even deeper insights of the portfolio, investment style and performance across market cycles among others. Aided with tables and easy-to-understand charts, PersonalFN’s FundSelect reports offer you value for money.

Only for a limited period, we are offering this exclusive service loaded with benefits. Don’t miss it. Subscribe now!

|

Add Comments

| Comments |

Sameer.khannas@gmail.com

Sep 11, 2019

Hi, pls call me on my number. |

1