Just a few weeks to go, and soon FY2017-18 will become the past.

As salaried employees, many of you may have already completed the annual income tax exercise of submitting the investment declaration and investment proofs to your employers.

For those who haven’t, there’s just three weeks left.

Don’t rush and make adhoc investments just to save tax. Remember, haste makes waste. Take little time out, do a little research, and then invest in suitable tax-saving products.

If year-end work pressure is cutting your time short, relax, this article is just for you.

Read further for some tax saving tips and suitable tax saving investments that can fulfill your needs.

If you are salaried, make optimal use of the allowances provided. Allowances such as House Rent Allowance (HRA), Leave Travel Allowance (LTA), and Medical Reimbursement, etc. can help you cut down on tax.

Some of you may have already provided proof of expenses under these allowances. However, if you have incurred additional expenditure in terms of travel or medical expenses, and have not fully utilised the limit provided, you can save a bit more on tax outgoes.

To know more on HRA, read: HRA Tax Implications: All You Need To Know

Now we head to the formidable Section 80C , of the Income Tax Act, 1961. I use the word formidable, because there are so many investment options and expenses covered under this Section, making it a daunting task for any individual.

In our experience, those who have money to spare, ignore the different options and invest the entire limit of Rs 1.50 lakh in a single product or a mix of few products such as PPF, Bank tax-saving deposits, tax-saving mutual funds or Equity Linked Savings Schemes (ELSS) etc.

[Check out PersonalFN’s Exclusive Report - 3 Tax-Saving Mutual Funds (ELSS) For 2018.]

This saves them the hassle of comparing different options or keeping multiple investment proofs. Though convenient, this may not be the best form of tax saving. It is merely a tax-saving exercise and not optimal tax planning.

Unlike “tax saving”, which is generally done through investments in tax saving instruments / products, “tax planning” takes into consideration the larger financial plan after accounting for age, financial goals, risk appetite, and investment horizon (including nearness to financial goals).

By adapting to this method of “tax planning”, you not only ensure long-term wealth creation, but protection of capital as well.

So, please remember to commence your “tax planning” exercise well in advance by complementing it with your overall investment planning exercise.

Do read: Everything You Need To Know About Tax Planning

It is never too late to plan. You still have time to make investments, in line with your financial goals, if you have not fully utilised the Rs 1.50 lakh limit under Section 80C.

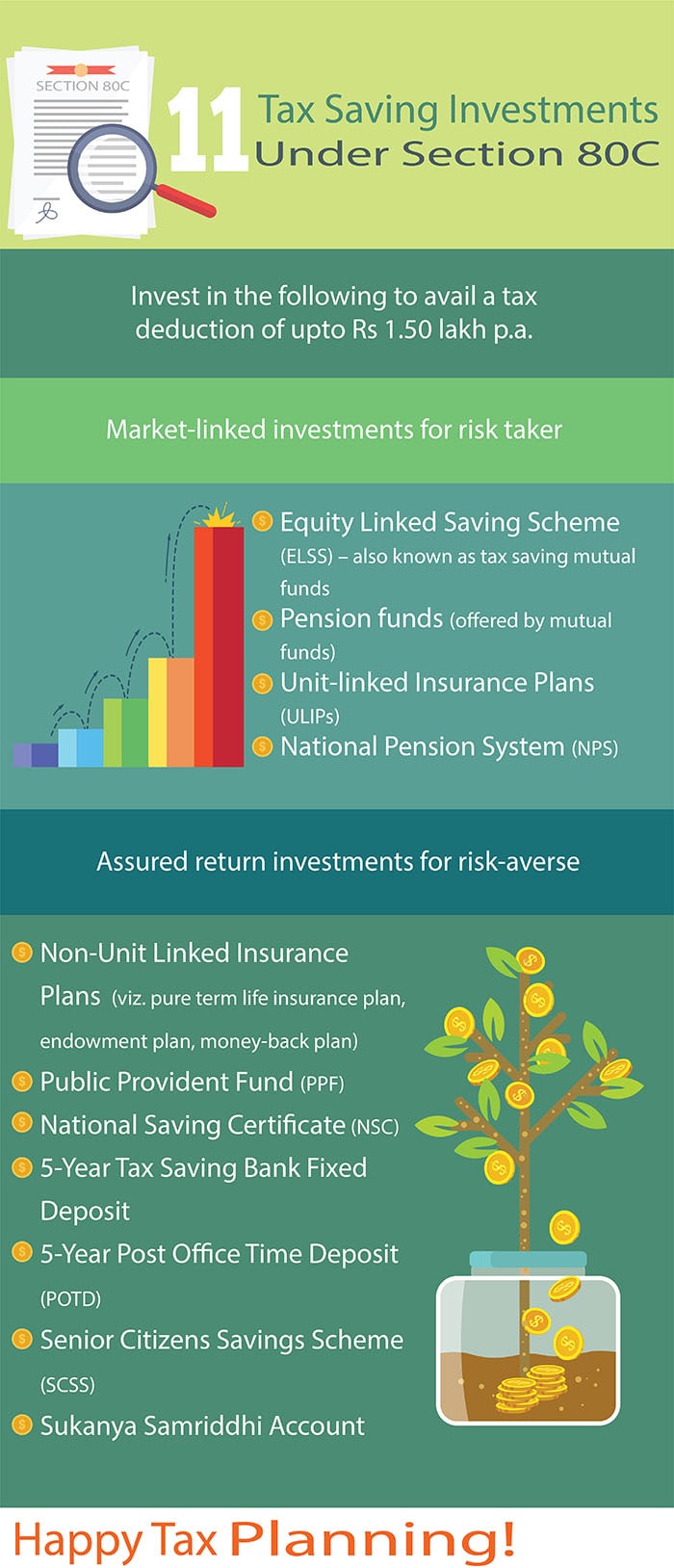

Here are the investment avenues available under Section 80C:

Apart from the investment avenues mentioned above, you can claim these expenses as well:

- Tuition fees paid for children’s education (maximum 2 children)

- Principal repayment on Housing Loan.

- Stamp Duty and Registration Charges

A must read: All You Need To Know About Section 80C

If you are seeking long-term wealth creation, then tax saving mutual funds or ELSSs will be the best route. Though the long-term capital gains are now taxable, they still are capable of delivering inflation-beating returns. Thus, ELSSs should form a vital part of your tax savings portfolio. Check out this short video for more-

How can I save on taxes with Mutual Funds?

Look beyond Section 80C

For many, tax planning starts as well as ends with Section 80C of Income-tax Act, 1961. However, investing only in these investment instruments will not optimally reduce your tax liability. There are many other options available apart from Section 80C, which you should look into. Thinking beyond 80C may help you save more for your other financial goals.

Section 80D: The premium paid by an Individual or HUF on medical insurance policy to cover your family (including spouse and children) and parents against any unexpected medical expenses, qualifies for a deduction under

80d 80D.

- Tax deduction on health insurance premium paid for you & your family

- Tax deduction on health insurance premium paid for your parents

- Tax deduction on preventive health check-up expenses

- Tax deduction on medical expenses of super senior citizens

| Individuals covered |

Exemption Limit |

Preventive Health Check-Up Expense |

Total |

| Self and family (self, spouse and dependent children) |

Rs 25,000 |

Rs 5,000 |

Rs 25,000 |

| Self & family + parents |

Rs 50,000 = Rs (25,000 + 25,000) |

Rs 5,000 |

Rs 55,000 |

| Self & family + senior citizen parents |

Rs 55,000 = Rs (25,000 + 30,000) |

Rs 5,000 |

Rs 60,000 |

| Senior citizen self & family + senior citizen parents |

Rs 60,000 = Rs (30,000 + 30,000) |

Rs 5,000 |

Rs 65,000 |

(Source: Personal FN Research)

In case you are non-senior citizen paying self, spouse, and dependent children, the maximum amount allowed annually as a deduction is Rs 25,000. And, if you are a Senior citizen paying health insurance premium for yourself, the maximum deduction is Rs 30,000.

So, if you pay medical insurance premium for your parents (irrespective of whether they are dependent on you or not), you can claim an additional deduction of upto Rs 30,000 in case your parents are senior citizens or Rs 25,000 in other cases under this section.

So, for example, if you pay a premium of Rs 15,000 for yourself and Rs 20,000 for your parents, you will be eligible for a total deduction of Rs 35,000 only, assuming your parents are not senior citizens.

For everything you need to know of Section 80D read: All You Need To Know About Section 80D

Other sections such as Section 80G, Section 80TTA, etc. can help you reduce the tax outgoes further.

Options Galore - Snapshot of deductions under different sections

| Section |

Short description of the deduction |

| 80E |

Interest on loan taken for pursuing higher education |

| 80G |

Donations to certain funds and charitable institutions |

| 80GG |

Rent paid in respect of property occupied for residential use/td> |

| 80GGA |

Certain donations for scientific research or rural development |

| 80GGC |

Contribution made to any political parties or electoral trust |

| 80TTA |

Deduction in respect of interest earned on savings bank deposits |

| 80U |

Person suffering from specified disability(s) |

Note: The list is not exhaustive, but only indicative

(Source: Personal FN Research)

Do use all the permissible deductions to save tax. And do submit your investment declaration proofs on time. Avoid procrastinating till the last minute, so don’t aimlessly invest in tax saving investments. It is important for you to know the various routes to save tax on your income.

As most employers deduct tax in the last quarter of the year based on investment proofs submitted earlier, there are chances of excess tax being deducted if you have made last minute investments.

Is your case?

Then, you can claim an income tax refund when you file your returns.

P.S. You can also download our latest exclusive Tax Planning Guide here. It will help you cross-check if you are on the right track of saving on taxes and to take timely action, in case you have missed any benefits.

| Editor’s Note:

Did you know, ELSS funds are an ideal investment avenue for high-risk investors to park their long-term funds and earn a tax rebate as well.

In terms of investment style, ELSS may be of any genre. They may follow growth or value style or even a combination of both. Moreover, they may restrict themselves to a particular market-cap or may invest without any market-cap bias.

ELSS funds are suitable for those with a high risk appetite. As an investor, you need to pick the right and suitable ELSS funds to meet your financial goals.

This is why my highly experienced research team at PersonalFN adopts a process that combines both quantitative and qualitative factors when shortlisting funds. This process, which has been perfected through the years, has a good chance of picking funds that can deliver decent market-beating returns.

If you are looking for the top ELSS funds to invest in 2018, I highly suggest you subscribe to PersonalFN’s Exclusive Report - 3 Tax-Saving Mutual Funds For 2018.

In this report, you will find the Top 3 ELSS that are geared to grow your investment multi-fold over the long term while saving your taxes. These Top 3 ELSS are handpicked through our special 7-point Selection Matrix methodology, and considered to be potentially the best tax-saving mutual funds in the Indian market.

|

Add Comments