(Image source: unsplash.com)

(Image source: unsplash.com)

Are you too young to plan your retirement?

If you think so, you are perhaps heading for a bumpy, ill-planned retirement.

Retirement is possibly the farthest financial goal in your life. But it's as important as any other goal such as buying a home or children education.

Other excuses people not planning for their retirement frequently give are:

If you have already chalked out an investment plan for your retirement, do you think you will retire rich?

Not necessarily. This is another myth.

Many among those who plan their retirement meticulously and well in time, often end up investing in wrong investment avenues.

Take example of Divya and Ranjan.

Divya and Ranjan's financial planner advised them to invest Rs 16,000 per month to take care of post-retirement expenses. While he didn't misguide them on the corpus they needed, he recommended the wrong products, for his under-the-table arrangement with a mutual fund broker and an insurance agent.

Divya is investing Rs 8,000 in a unit-linked retirement plan offered by an insurance company. While Ranjan is investing an equal amount in a retirement fund offered by a mutual fund house.

Unfortunately, Divya and Ranjan are investing in (so called) readymade retirement planning solutions. But the reality they are investing in products that are absolutely unnecessary and can be done away with completely.

[Read: Can You Solely Depend On 'Retirement Funds' For Your Retirement? ]

Then where should they invest?

Mutual funds offer a variety of schemes under various categories. Majority of investors won't need any fancy product, if they choose not only the mutual fund schemes but also the mutual fund categories wisely while planning their retirement.

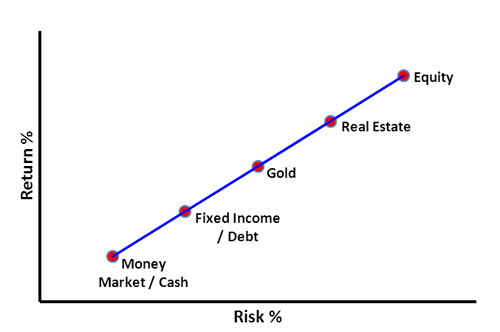

In retirement planning, asset allocation is the most important decision, not the product selection. For those who haven't heard this phrase, asset allocation is nothing but the proportion in which you hold various assets such as equity, fixed income (debt), gold, and real estate in your portfolio.

Please remember risk and return go hand in hand. If you invest in fixed income assets, you might be exposed to lower risk, but returns would be lower too. As against this, if you invest in equity mutual funds, you would assume high risk but returns would be correspondingly high too.

Risk-return equation of various asset classes

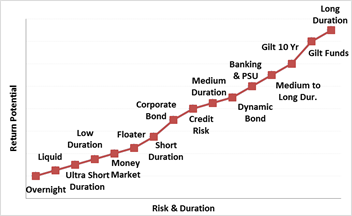

Mutual funds help you invest across asset classes. If you are investing in debt through mutual funds, you can choose a mutual fund category depending on your risk appetite and time horizon. If you have a low risk appetite, you should avoid investing in dynamic bond funds and long duration funds even though interest rates in the economy are set to fall. Similarly, those with shorter investment horizon shall also avoid investing in these fund categories even though their risk appetite might be high.

[Read: Why You Should Not Ignore Personalized Asset Allocation While Investing]

Risk-return spectrum: debt

By now you must have understood by now that risk appetite and duration equally influence the category you invest in. Hence, if you invest in long duration funds for the retirement planning purpose or dynamic funds or medium to long duration funds, don't allocate more than 20% of debt-portion in your portfolio. Remember, debt funds are not risk -free.

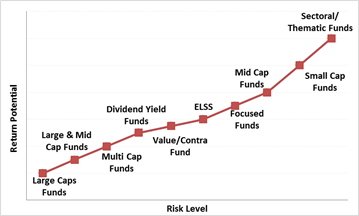

Risk-return spectrum: equity

Speaking about equity oriented mutual funds, large cap funds are the safest among equity funds. Reminder: equity is the most volatile and hence the riskiest asset class. Small cap funds are the riskiest diversified equity funds, whereas, sectoral and thematic funds are the riskiest equity funds.

To counter volatility and avoid the need to time the market, you should prefer Systematic Investment Plans (SIPs). Moreover, investing in direct plans helps you accelerate your returns.

While creating a portfolio for your retirement, you can invest 5%-10% of your investable corpus in gold. Gold Exchange Traded Funds (ETFs) is one of the most viable options to invest in gold in paper form. Nonetheless, you can also invest in gold savings funds which are nothing but the Fund of Funds (FoF) schemes investing in Gold ETF(s).

Indicative allocation to various mutual fund categories

| Age Group |

25-35 |

35-45 |

45-55 |

55-60 |

Above 60 |

| Category |

Very Aggressive |

Aggressive |

Moderate |

Conservative |

Very Conservative |

| Equity |

90%-100% |

75%-80% |

60%-70% |

40%-50% |

20%-30% |

| Large Cap Funds |

10%-15% |

10%-15% |

10%-15% |

15%-20% |

10%-15% |

| Midcap Funds |

20%-25% |

15%-20% |

-- |

-- |

-- |

| Large & Midcap Funds |

20%-25% |

15%-20% |

10%-15% |

-- |

-- |

| Multi Cap Funds |

15%-20% |

15%-20% |

10%-15% |

-- |

-- |

| Value Style Funds |

15%-20% |

10%-15% |

10%-15% |

10%-15% |

0%-10% |

| Aggressive Hybrid Fund |

-- |

-- |

10%-15% |

15%-20% |

10%-15% |

| Debt |

0%-5% |

10%-15% |

20%-30% |

40%-50% |

70%-80% |

| Dynamic Bond Funds |

0%-5% |

10%-15% |

10%-15% |

20%-25% |

15%-20% |

| Short Duration / Corporate Bond Funds |

-- |

-- |

10%-15% |

20%-25% |

25%-30% |

| Liquid / Ultra Short Duration Funds |

-- |

-- |

-- |

0%-10% |

20%-30% |

| Gold |

0%-5% |

5%-10% |

5%-10% |

5%-10% |

0%-5% |

| Gold Funds |

0%-5% |

5%-10% |

5%-10% |

5%-10% |

0%-5% |

|

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

This table is for illustration purpose only.

(Source: PersonalFN Research)

While you refer to the table above when creating your retirement portfolio, you may like to consult a financial advisor to make it more personalised. The above table is only for the illustration purpose. It may or may suit you depending on your risk appetite and existing financial circumstances.

Key takeaways for investors:

While planning your retirement through mutual funds, you should always be careful about the selection of a mutual fund category. Selecting a right scheme comes later. You should consider both qualitative and quantitative factors while choosing a right scheme for your portfolio.

Editor's note: If you want your retirement to be blissful, don't miss out on PersonalFN's Retire Rich service. This is a new and exclusive service with the sole intent of securing your retirement.

It is a DIY (Do It Yourself) retirement solution, whereby you can start planning for your retirement and potentially build a substantial corpus that could sustain you in the golden years of your life.

It is not merely a list of funds or a particular investment idea. It is a comprehensive solution to guide you with almost ALL the necessary essentials of retirement planning. Subscribe now!

Add Comments