| S&P BSE Sensex* |

Re/US $ |

Gold Rs/10g |

Crude ($/barrel) |

FD Rates (1-Yr) |

34,848.30 |-687.49

-1.93% |

67.70 |-0.45

-0.67% |

30,830.00 | -431.00

-1.38% |

77.47 |3.85

2.75% |

5.0% - 7.0% |

Weekly changes as on May 17, 2018

BSE Sensex value as on May 18, 2018

Impact

Geezerhood is an inescapable truth of life. In a way, old age can be a two-way sword. If you have done a lot of good work in your young age, retirement becomes a time to relax and celebrate the last phase of life. For any reason if you made wrong choices when you’re young, you might have to pay for them at a later stage in life.

Signs of a peaceful retired life:

✔ Good health

✔ Sound financial condition

✔ Supportive friends and family

✔ A hobby

✔ And contentedness

The opposite of each of the above can make your retirement extremely distressful. Believe it or not, the factors given above are so much important (perhaps in that order) for your peaceful retirement.

Have you ever asked yourself, if you are doing enough to ensure you will have a good life even in your old age?

Do you take care of your health?

Do you have any lifestyle diseases?

Do you save enough and invest wisely?

Do you draw a line to your ambitions?

Do you give enough time to your family and friends? And more importantly, do you have any hobby that can keep you busy once you hang up your boots?

A survey stated, many suddenly find it difficult to utilize the free time and get frustrated without the usual routine after retirement.

If you think you will do all of this “when it is needed” might be the biggest mistake of your life.

Your present habits decide the quality of your tomorrow’s life.

Have you ever bothered yourself to check your money habits?

Until recently, Vaibhav didn’t care how his lifestyle was affecting his expenses, nor about his poor financial decisions, and his complete ignorance towards family for a thriving career.

Last month, he needed a few lakh Rupees urgently. He checked his portfolio to quickly liquidate some of his investments. Perhaps, for the first time he reviewed his investments thoroughly.

He realised after eight years of doing investments, his so called “retirement funds” were performing miserably and giving him compounded annualised returns of under 6%. He had invested in 3-4 retirement plans offered by various insurance companies. He had fallen for their emotional appeal.

Vaibhav, a technology expert, earns a big fat salary. At 40, with all the luxuries of life, the only problem he faces today is his meager bank balance.

After looking at the performance of his investment, he got tensed. Will I be able to sustain my current life style after 15 years, once I retire? — he’s wondering now.

He’s trying to find a solution to a problem which is self-inflicted and could have been avoided completely in first place.

Moral of the story: Don’t get swayed away by the tall promises of marketers, instead do some hard work to find out what works for you in the long run.

What’s the right approach to planning your retirement?

✔ Know Your Expenses (KYE)

✔ Factor in the impact of inflation

✔ Estimate the amount you might need per month post retirement

✔ Estimate the corpus you need to have at your retirement

✔ Based on your risk appetite and return expectation estimate the investments you might have to do per month until retirement

✔ Review your investments periodically

Assume you need Rs 50,000 per month and expect to maintain the same lifestyle post retirement, say after 20 years. If inflation goes up by 5% every year, your monthly expenses would be 1.35 lakh per month at your retirement, i.e. at 60.

Suppose your investments generate 1% inflation and tax - adjusted returns on your retirement kitty post retirement, you will need Rs 2.95 crore at your retirement, assuming a life expectancy of 80.

You will have to save Rs 6.44 lakh every year for 20 years to build the retirement corpus you require. If you had started five years earlier, you would need to save approximately Rs 4 lakh a year.

Now, let’s modify this a bit.

If you can generate 10% returns for 25 years, the investment of Rs 3 lakh per year would also suffice.

You see, there’s no option to starting early and investing wisely.

Some of you might ask which investment avenue would generate 10% returns for 25 years.

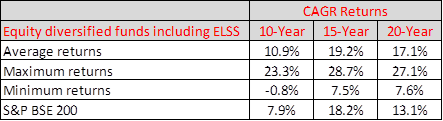

To your surprise, on an average, equity diversified mutual fund schemes, including Equity Linked Savings Schemes (ELSS), have generated 17.1% Compounded Annualised Growth Rate (CAGR) returns over last 20 years. The lowest returns generated by a diversified equity scheme have been 7.6% CAGR and 27.1% have been the highest.

Mutual Funds…a right way to approach your retirement?

Data as on May 17, 2018

(Source: ACE MF ,PersonalFN Research)

Starting a few SIPs (Systematic Investment Plans) in diversified equity funds would be a good retirement planning option.

Do you face a difficulty in shortlisting mutual fund schemes for your portfolio?

Don’t worry!

PersonalFN’s Money Simplified Guide - 10 Steps to Select Winning Mutual Funds is an extremely valuable resource.

In this guide you will find…

✔ Why is it necessary to hold winning mutual funds

✔ How to compare performance of mutual fund schemes

✔ What to look for in a fund’s portfolio

✔ How to judge the competence of the fund house

✔ How to analyse fund managers skills

✔ Steps to build a solid mutual fund portfolio

Many of you might not have the time, expertise, or both to select mutual fund schemes on your own. If you are one of them, don’t lose heart because PersonalFN’s unbiased mutual fund research service—FundSelect is just meant for people like you.

Every month, PersonalFN’s FundSelect service will provide you with an insightful and practical guidance on equity funds and debt schemes – the ones to buy, hold, or sell. Thus assisting you in creating the ultimate portfolio that has the potential to beat the market.

PersonalFN has a dependable track record and has guided investors achieve their envisioned financial goals with their unbiased views.

PersonalFN does not take shortcuts with its research before recommending mutual fund schemes to investors. A comprehensive rating methodology is followed.

Thousands of data points are analyzed to shortlist best mutual fund schemes by using a host of quantitative and qualitative parameters.

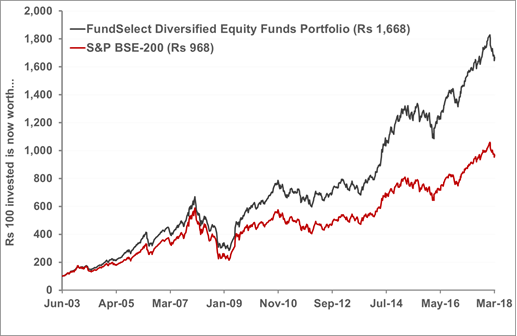

PersonalFN's Mutual Fund Research service 'FundSelect' Vs. S&P BSE 200

Data as on March 28, 2018

(Source: ACE MF, PersonalFN Research)

Out of every four funds recommended in the FundSelect, three have always outperformed BSE 200 index. That's the success rate of PersonalFN.

FundSelect is turning FIFTEEN.

On this auspicious 15th anniversary of FundSelect, we intend to make it “ultra-special” for you.

How?

Well, how about getting 1-Year of access to FundSelect virtually Free?

And there’s MORE...

Get FREE access to our premium report, 'Top-5 Funds For 2020

So, hurry and subscribe to PersonalFN's FundSelect NOW!

If you wish you to chart a thorough retirement plan and follow it, Schedule a Call with our financial planner or even drop a mail at info@personalfn.com and we will get in touch with you. We would be happy to plan your finances prudently to help you achieve your life goals.

PersonalFN is a SEBI registered investment advisor.

Happy Planning!

Happy Investing!

MustRead

Are These Top Large Cap Mutual Funds Worth Your Investment in 2018?

Don't Just Read About Mutual Funds. Make A Profit With That Learning

Impact

Since you are reading this post, we assume you either invested in mutual funds or you would soon want to start investing.

If you already invest in mutual funds, you are perhaps looking to accelerate your returns and understand mutual funds in a better way.

Naïve investors may not be even sure about their starting point.

To read more please click here.

Invest In Direct Plans Of Mutual Funds. Here's The Best Approach To Do That…

Impact

If you invest in mutual funds, you should opt for Direct Plans.

Does this sound too repetitive?

Well, it may.

Time and again we have been advising our dear readers to opt for only Direct Plans when investing in mutual funds, because lower expense ratio of Direct Plans can add significant wealth in the long run.

To read more please click here.

Smart & Advance Way To Start SIPs For Your Child's Financial Future

Impact

Are you serious about your children's future?

Of course, I am.

Was this your response?

Please don't get annoyed by the question.

The intent of raising it now wasn't to hurt you.

Quite often it happens that, despite having a good purpose, we end up doing ordinarily in the end.

To read more please click here.

FUND OF THE WEEK

ICICI Prudential Dynamic Plan Will Now Be A Multi-Asset Fund – All You Need To Know

Franklin India Prima Plus is one of the flagship schemes of Franklin Templeton Mutual Fund. Launched over two decades ago, this large-cap biased fund has attained a corpus of over Rs 10,000 crore. Now that SEBI has issued norms for mutual fund scheme categorization, the fund house had to make changes in the scheme to comply with the regulations.

Since, Franklin India Prima Plus predominantly invests in large-cap stocks with an opportunistic allocation to mid-caps (15%-20%), the fund house had an option to categorise the fund under one of the following categories – Large Cap Fund, Multi Cap Fund or a Large & Mid Cap Fund.

Tutorials…

All You Need To Know About Equity Mutual Funds

Financial Terms. Simplified.

Credit Quality: Credit quality is one of the principal criteria for judging the investment quality of a bond or bond mutual fund. As the term implies, credit quality informs investors of a bond or bond portfolio's credit worthiness or risk of default. A company or security's credit quality may also be known as its "bond rating.

(Source: Investopedia)

Quote: "Investment is most intelligent when it is most businesslike.”‒Benjamin Graham