| S&P BSE Sensex* |

Re/US $ |

Gold Rs/10g |

Crude ($/barrel) |

FD Rates (1-Yr) |

34,056.83 |116.53

0.34% |

64.06 |0.04

0.06% |

29,245 | 605.00

2.11% |

66.19 |1.99

3.10% |

5.00% - 6.75% |

Weekly changes as on December 28, 2017

BSE Sensex value as on December 29, 2017

Impact

At the end of 2016, not many investors in India were in a party-mood. Demonetisation followed by a sharp decline in the equity indices had shattered investors’ hopes. Many experts and market commentators had painted gloomy picture of the prospects

in the aftermath of note ban. The global investment climate wasn’t supportive either. Mr Donald Trump becoming the President of the US was considered to be a major event that could potentially, and perhaps permanently, affect the globalisation trends and the fate of cross-country treaties. No wonder, the year 2017 had started on a jittery note for the markets across the globe. Nonetheless, as they say,

all’s well that ends well.

Strong performance of equities all-around…

| Index(Market) |

Year-To-Date returns

|

| Merval (Argentina) |

72.6% |

| BIST 100 (Turkey) |

43.5% |

| Hang Seng (Hong Kong) |

34.5% |

| Santiago IPSA (Chile) |

29.0% |

| S & P BSE Sensex (India) |

27.4% |

| Sao Paulo Bovespa (Brazil) |

26.3% |

| Dow Jones Global Index (World) |

21.6% |

| Kospi (South Korea) |

20.2% |

| S&P 500 Index (The U.S.) |

19.8% |

| Straits Times (Singapore) |

17.7% |

| DAX (Germany) |

13.8% |

| CAC 40 (France) |

10.4% |

| IBEX 35 (Spain) |

8.7% |

| FTSE 100 (U.K.) |

6.7% |

| Shanghai Composite (China) |

5.5% |

| RTS Index (Russia) |

-0.3% |

Data as on December 27, 2017

(Source: The Wall Street Journal)

As we are near the fag end of 2017, it’s safe to assume that the investors would shut shop for 2017 with hefty gains. With a little over 27% gains so far on S&P BSE Sensex—India’s widely tracked index—Indian markets found place among the world’s most attractive equity markets in 2017.

Factors that contributed in the relative outperformance of Indian markets...

Market rally started on a low base: Sharp market sell-off that happened post demonetisation had made stock valuations comfortable. In the subsequent time, the economy recovered faster than anticipated earlier and many companies across the industries posted stable quarterly results. As a consequence, markets quickly took the corrective action and climbed to pre-demonetisation levels and soon surpassed. Therefore, to put it more precisely, the large-part of outperformance of Indian markets in 2017 stems from relative underperformance of Indian equities in the last two months of 2016.

Lacklustre Performance of other assets: Over last few years major asset classes such as gold and real estate have failed to make a mark. As investors tend to focus more on the recent performance of the asset class before investing in it, new investment in these assets classes dried up in 2017 and got diverted to equity markets.

Domestic Institutional Investors (DIIs)- driven rally: From the beginning of 2017 until December 26, 2017, DIIs poured in massive Rs 91,354 crore. As against that, Foreign Institutional Investors (FIIs) remained net sellers. Putting Cash and Derivatives market numbers together, the net outflows of FIIs during the same time period stood at Rs 79,494 crore.

In other words, DIIs inflows more than offset FII outflows, thereby pulling up the markets along.

Systematic Investment Plans (SIPs) gained attention of individual investors. In January 2017, mutual funds collected Rs 4,095 crore under SIPs. The contribution of SIPs in the DII investments rose steadily throughout 2017. In November 2017, SIPs gathered Rs 5,893 crores. Average Monthly SIPs upto November in 2017 stood at Rs 4,842 crore.

(Source: AMFI)

Union budget offered a fillip to the market: Budget 2017-18 reaffirmed the Government’s commitment to improving the state of infrastructure in the country. The allocation to infra and allied sectors jumped to Rs 3.96 lakh crore. More importantly, the Government showed no intent to deviate substantially from the path of fiscal discipline. As a net effect, investors lapped up shares of companies that were expected to be benefited by the Government spending.

Changing political equations: After the victory of the Bharatiya Janata Party (BJP) in the UP elections and distinctive triumphs in other major states, except Punjab, markets were enthused. The shift in the political power boosted confidence of investors who were hopeful of the Government’s ability in implementing various reform programmes more efficiently had the agenda of State Governments and that of the Centre well-aligned.

Having the same ruling party in the Centre and major states of the country makes a significant difference in the pace of implementation of critical reforms. Moreover, the markets sensed some long-stuck legislative Bills getting cleared in due course with improving tally of the ruling party and its allies in the Rajya Sabha.

Recapitalisation hopes: Towards the end of 2017, Government decided to

deal with the problem of Non-Performing Assets (NPAs) conclusively. It intends to infuse massive Rs 2.11 lakh crore over next two years. As equity investors witnessed the unfolding of this and other related events, they showed greater trust in Public Sector Banks (PSBs) and accumulated stocks of PSBs sending the indices northwards.

And what pushed the markets down?

The markets were on the tenterhooks when the Government implemented one of India’s biggest ever indirect tax reforms—Goods and Services Tax (GST). Temporary hiccups caused during the transitionary phase made markets worried. Moreover, geo-political tensions and the political aggression on the Korean Peninsula made markets vulnerable.

What to expect in 2018?

The US Federal Reserve (Fed) raised interest rates thrice times during 2017 backed by signs of economic vigour depicted by the economy. This attracted capital flows to the US. At the moment, the global investors seem to be more optimistic about the global growth than worried about the rising inflation.

S&P 500 rising nearly 20% in a calendar year isn’t a routine event. The historical average returns in a calendar year are close to 8%. In 2018, the earnings are likely to pick up —thanks to tax cuts. Strong performance of the U.S. markets largely decides the direction of global capital flows.

The Fed is expected to hike interest rates 3-4 times in 2018. Which may suck off some flows which otherwise may find their way to emerging markets. Nonetheless, inflows to emerging markets are still well-below 25% from their 2013-highs.

What does it mean to Indian markets?

So far, Indian equity markets haven’t felt the heat of monetary policy normalisation in the advanced nations, primarily because of unabated domestic inflows.

However, any global event rattling the investors’ sentiment may quickly reverse this trend, particularly when the valuations seem stretched (across market capitalisation) vis-à-vis earnings data. If FII flows glide to another coast, another investment destination, this will have a bearing on the Indian equity market, unless DIIs continue to participate aggressively as at present. Corporate earnings growth and Union Budget 2018-19 are some of the key elements for the future trajectory of the Indian equity market.

So, while you step into 2018 on hopes don’t get swayed by exuberance and going gung-ho. It’s best to take note of the famous quote “Be fearful when others are greedy and greedy when others are fearful,” by legendary investor, Warren Buffett.

During such times it is imperative to strategically structure or review your portfolio based on your asset allocation.

PersonalFN therefore recommends that you follow a ‘core and satellite approach’ to investing. Here are 6 benefits of ‘core and satellite approach’:

- Facilitates optimal diversification;

- Reduces the risk to your portfolio;

- Enables you to benefit from a variety of investment strategies;

- Aims to create wealth cushioning the downside;

- Offers the potential to outperform the market; and

- Reduces the need for constant churning of your entire portfolio

‘Core and satellite’ investing is a time-tested strategic way to structure and/or restructure your investment portfolio. Your ‘core portfolio’ should consist of large-cap, multi-cap, and value style funds, while the ‘satellite portfolio’ should include funds from the mid-and-small cap category and opportunities style funds. But what matters the most is the art of astutely

structuring the portfolio by assigning weightages to each category of mutual funds and the schemes you select for the portfolio. Moreover, with change in market outlook the allocation/weightage to each of the schemes, especially in the satellite portfolio need to change.

To

pick mutual fund schemes for your portfolio, prefer the ones that have proven their mettle, so as to have only the consistent ones in your mutual fund portfolio. Prefer those which follow robust investment processes and systems as against those indulging in momentum playing.

Further, have a long-term investment horizon in mind, of at least 5 years. A staggered approach to investing as valuations appear pricey would be prudent. Those who are new to equity investing or even seasoned prefer the mutual fund route by opting for diversified large-cap equity funds and/or

ELSS (also known as tax saving funds) now amid the tax saving season.

Opt for the

Systematic Investment Plan (SIPs) and/or Systematic Transfer Plan (STP) mode of investing. This will help you to mitigate the risk better. Thoughtlessly investing or speculating can be hazardous to your wealth and health. Even while buying stocks, choose them carefully.

If you’re looking at high investment gains at relatively moderate risk,

PersonalFN’s latest offering: The Strategic Funds Portfolio For 2025 is perfect for you! In this report, PersonalFN will provide you with a readymade portfolio of its top recommended equity mutual funds schemes for 2025 that have the ability to generate lucrative returns in the long run.

How To Deal With The Falling Interest Rates On The Small Savings Schemes?

Impact

At a time when

equity markets are generating awe-inspiring returns for investors who can take risk; conservative or risk-averse investors are unable to hide their frustration with

falling interest rates.

The latest in the list of fixed income assets to offer lower returns are the Government-run Small Savings Schemes (SSS) such as Public Provident Fund (PPF), National Savings Certificate (NSC) and Kisan Vikas Patra (KVP) among others. The Government reduced the interest rate on SSS by 20 basis points (bps) or 0.2 percentage points for the Q4 of FY 2017-18 (i.e. for January-March quarter). For the Q3 FY 2017-18, the Government had left the interest rates on SSS unchanged. As you might be aware, the Government adopted a policy of quarterly interest rate revision from the beginning of FY 2016-17.

Across the board fall in the interest rates…

|

Small Saving Scheme

|

Interest rates |

|

Old

|

New

|

| PPF |

7.8% |

7.6% |

| NSC |

7.8% |

7.6% |

| KVP |

7.5% |

7.3% |

| Sukanya Samriddhi Account |

8.3% |

8.1% |

| #Post Office Time Deposits less than 1 to 5 yrs |

6.8%-7.6% |

6.6%-7.4% |

| 5-year Post Office Time Deposit |

7.1% |

6.9% |

| Post office Monthly Income scheme |

7.5% |

7.3% |

| Senior Citizen Savings scheme |

8.3% |

8.3% |

#For the maturity of 1-year to 5-year

(Source: India Post, Finance Ministry Notification)

It seems despite interest rates linked to the market driven yields on sovereign securities of the concurrent maturities, the Government is administering the interest rates keeping in mind a lot of other factors. For example, when yields were falling in Q2 FY 2017-18, the Government preferred not to lower the interest rates. This raises the doubt if it was done to avoid the wrath of the common man before going in for crucial state elections.

Can interest rates fall further?

While it’s beyond anybody’s guess, primary analysis suggests that there isn’t much room left for interest rates to slide. Inflation is steadily inching up. In fact, with the dual impact of rising food prices and implementation of the Seventh Pay Commission, inflation is expected to remain in the range of 4.3% to 4.7% in the second-half FY 2017-18, i.e. between October 2017 and March 2018. In the first-half of the FY 2017-18, i.e. between April 2017 and September 2017; the retail inflation averaged below 3.0%. Under such a scenario, RBI is unlikely to accord any rate cut. As it appears, the Government is following the yields with a lag to decide the

interest rates on SSS.

What investors should do?

Some SSS such as PPF and NSC offer you a benefit of compound interest. Therefore, despite the relatively low rates, they cannot be ignored if you are risk-averse or shorter investment horizon. But make sure you invest your hard-earned money in SSS as per your

Asset Allocation and as

Personalised financial plan can help you decide on the amount you should commit to these schemes.

Why Is The Rise In Mutual Fund AUM Worrying RBI? Know Here…

Impact

Monetary policies in advanced countries are returning to normalcy. And across the globe, they are adequately accommodative to maintain liquidity.

On home turf, the liquidity position is comfortable—thanks to demonetisation, which drew idle domestic savings into the organised system. Easy liquidity in the global and domestic markets is causing infrequent inflows in the Indian capital markets.

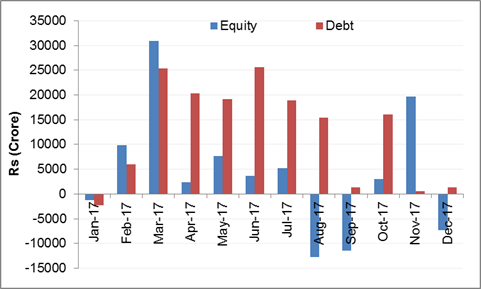

Foreign Portfolio Investments in Indian capital markets…

Data as on December 17, 2017

(Source: CDSL, PersonalFN Research)

The Reserve Bank of India (RBI) recently released the 16th edition of Financial Stability Report (FSR) — a bi-annual publication. It assessed the stability of India’s financial system with respect to risks emerging from global and domestic factors.

To read more about this story and Personal FN’s views over it, please click here.

Here’s What The EPFO Is Planning In 2018…

Impact

The Employees’ Provident Fund Organisation (EPFO) is on its way to transforming itself into an

investor-friendly organisation. In 2017, it took some well-disposed decisions, which included simplifying the process of withdrawal, claim settlement, and allowing easy portability of

EPF accounts. It also started the delivery of a range of services through digital means.

Recently, EPFO also

decided to credit the units of equity ETF (Exchange Traded Funds) directly to investors’ accounts. Until then, the benefits of equity investments didn’t reflect in the interest rate calculation or in the subscriber’s account. As you know, the

EPFO passively invests upto 15% of the in equity markets through the ETF route.

In 2018, India’s largest

retirement money manager aims to go entirely digital and use Aadhaar to raise the quality of its service standards..

To read more about this story and Personal FN’s views over it, please click here.

Can The Idea Of Permanent Mutual Fund Portfolio Ever Work? Know Here

Impact

Have you heard of a pill that will keep you happy and healthy forever?

No?

Well, neither have we.

We hope you remain in the pink of health always.

But, on the occasions when you feel unwell, a trip to the doctor is usually recommended. Based on the diagnosis, the reputed medical practitioner will prescribe medication to get you back in good health. Naturally, the medication differs depending on the type of illness.

Even if you are in the best of health, many recommend a routine health check-up to ensure your body can withstand other diseases.

Just like your physical health, your financial health also needs to remain always in the pink.

When you begin investing, it is important to assess financial goals—both the amount of return required and the risk tolerance. Once that exercise is completed, investing should not be a “

set it and forget it” exercise.

You need to look far into the future and make several assumptions when planning investment goals. But, in reality, markets can change quickly. A market crash has the capability to wipe out a significant portion of your wealth.

To read more about this story and Personal FN’s views over it, please click here.

And Other News...

Fortunately, machines haven’t started asking for “under the table arrangements” for carrying out tax assessments—unlike rough tax officials. Perhaps, that’s the reason why, the Prime Minister urged for pushing faceless and nameless assessment process that he believes would lower the instances of corruption and extortion of money. The Government is expected to make some announcement in this regard in the forthcoming Budget. Nonetheless, the decision of choosing e-assessment or the manual assessment will be at the discretion of the assessee.

Tutorials…

How To Claim Unclaimed Money Of Your Mutual Funds

Bank FDs vs. Debt Mutual Funds: Which is better?

5 Deterring Points About National Pension Scheme

How To Invest In Mutual Funds Online

Financial Terms. Simplified.

Risk-On Risk-Off: Risk-on risk-off is an investment setting in which price behavior responds to and is driven by changes in investor risk tolerance. Risk-on risk-off refers to changes in investment activity in response to global economic patterns. During periods when risk is perceived as low, risk-on risk-off theory states that investors tend to engage in higher-risk investments; when risk is perceived as high, investors have the tendency to gravitate toward lower-risk investments.

(Source: Investopedia)

Quote: Great investment opportunities come around when excellent companies are surrounded by unusual circumstances that cause the stock to be misappraised."- Warren Buffet