(Image source: pixabay.com)

(Image source: pixabay.com)

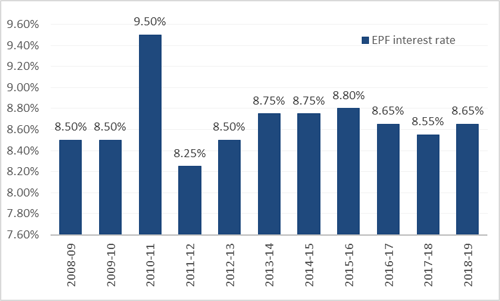

What a pleasant surprise for EPFO subscribers. This was unexpected, as the EPFO was expected to retain the interest rate of 8.55% for FY 2018-19.

Chart: How have interest rates on EPF moved?

(Source: EPFO, PersonalFN Research)

Professionals in the organised sector are likely to benefit should the finance ministry give the go-ahead to the EPFO's recommendation. However, this would leave the organisation with a surplus of only 151 crore, which is the lowest amount in five years. In FY 2017-18, the retirement fund body had a surplus of Rs 586 crore.

Some media houses have called this move a pre-election populist measure aimed at winning over voters.

A hike of 10bps in the EPF interest rate doesn't look unreasonable, considering RBI's policy rate action in FY 2018-19. In FY 2018-19 so far, the RBI has increased the repo rate twice by 25bps each and has reduced the rate once by 25 bps. Thus, the net change has been 25 basis points in FY 2018-19.

From the beginning of FY 2018-19 until September, the yield on India's 10-year bond rose sharply, however it fell at an equally brisk pace thereafter. Hence, the net change in India's benchmark bond yields remained flat.

Unlike, that on other Small Savings Schemes (SSS), the interest rate on EPF is reshuffled only once a year. In other words, it comes with a real lag. Hence a hike of 10bps doesn't look like a populist measure.

Last month, the government had hiked interest rates on Public Provident Fund (PPF) and other SSS such as National Savings Certificate (NSC) upto 40bps. Despite this, EPF still remains the most lucrative government-backed investment avenue.

Is EPF the best retirement planning investment avenue?

As you might be aware, investments in EPF enjoy the EEE (Exempt-Exempt-Exempt) status from the taxation viewpoint. Meaning, the amount you invest in EPF helps you save tax, interest earned on EPF is also exempt from tax and proceeds too are tax-free at maturity or even otherwise.

As a result, many salaried people consider EPF as one of the most dependable retirement savings avenues.

But it's time to realise that EPF is not the only alternative.

Relying solely on EPF for building your retirement savings corpus isn't a wise move. On the contrary, you should try to estimate the amount you might need to live a tension-free life post-retirement.

Have you ever calculated how much you would probably save for your retirement solely through EPF?

Use PersonalFN's EPF calculator.

It is a one-step solution to all your EPF related calculation questions. It quickly calculates the return on your EPF contribution within no time. EPF Calculator is an online tool and is accessible from anywhere at any time.

What's the right approach to retirement planning?

Step #1: Determine the Retirement Corpus

Step #2: Start Early, and Retire Peacefully

Step #3: Follow your Asset Allocation

Step #4: Ensure you are optimally insured for life and health

Step #5: Track and review your plan periodically

[Read: Step-By-Step Approach To Retirement Planning]

Importance of asset allocation in retirement planning

In retirement planning, asset allocation is the most critical decision, not product selection. For those who haven't heard this phrase, asset allocation is nothing but the proportion in which you hold various assets such as equity, fixed income (debt), gold, and real estate in your portfolio.

Please remember risk and return go hand-in-hand. If you invest in fixed income assets, you might be exposed to lower risk, but returns would be lower too. You might be running this risk if you depend entirely on EPF for building retirement savings.

Hence, depending on factors such as years left to retirement, your existing retirement corpus, retirement saving you need to accumulate, and risk appetite, you can invest in various asset classes such as equity, gold, and real estate, besides fixed income.

Role of mutual funds in retirement planning

Mutual funds help you invest across asset classes.

If you are investing in debt through mutual funds, you can choose a mutual fund category depending on your risk appetite and time horizon. If you have a low-risk appetite, best avoid investing in dynamic bond funds and long duration funds although interest rates in the economy are set to fall. Similarly, those with shorter investment horizon should avoid investing in these fund categories even though their risk appetite might be high.

As against this, if you invest in equity mutual funds, you would assume high risk but the returns would be correspondingly high too.

Large cap funds are the safest among equity funds, while small cap funds are the riskiest diversified equity funds. And sectoral and thematic funds are the riskiest equity funds.

To counter volatility and avoid the need to time the market, you should prefer Systematic Investment Plans (SIPs).

A Systematic Investment Plan enforces a disciplined approach towards investing. SIPs work on the simple principle of investing regularly which enable you to build retirement corpus over the long-term.

SIPs help you average out your costs without making you time the market. Moreover, investing in direct plans enables you to accelerate your returns.

While creating a portfolio for your retirement, you can invest 5%-10% of your investible corpus in gold. Gold Exchange Traded Funds (ETFs) is one of the most viable options to invest in gold in paper form. Nonetheless, you can also invest in gold savings funds which are nothing but the Fund of Funds (FoF) schemes investing in Gold ETF(s).

If you plan your retirement systematically and well in advance, you won't have to depend on government's mercy. Under such a scenario, an interest rate hike of 10bps would be a welcome step for you but a reduction of 10bps may not disturb you much.

Editor's note: Looking for an easy and ready-made solution for your retirement? Choose Retire rich service, a comprehensive guide to plan for your retirement and potentially build a substantial corpus.

It is a DIY (Do It Yourself) retirement premium service to guide you with almost ALL the necessary essentials of retirement planning. In short, this is a new and exclusive service with the sole intent of securing your retirement. Subscribe now!

Add Comments