(Image source: freepik.com )

(Image source: freepik.com )

I'm an IT professional, who is a novice to the world of mutual fund investing. I came across the Mutual Funds Sahi Hai ad, which helped me recognize the long-term benefits of mutual funds. Of late, I'm reading about mutual funds.

I want to plan for my daughter's higher education needs (post-graduation expenses). Am I making an appropriate choice by considering mutual funds? If yes, which are the types of mutual fund schemes I should add to my portfolio? My daughter is currently 5 years of age and I'll need the money to fulfil the goal when she turns 21.

- S. Ramnath

Mutual fund schemes are definitely an apt choice for short-term savings to long-term wealth creation. Mutual funds offer diversification (gets you exposure to a variety of instruments and investment styles); you can invest a smaller investment surplus; deploy money efficiently via SIP/STP/SWP; it lowers your cost of investing; offers liquidity; and your hard-earned money is managed by professionals.

So, you are right in considering mutual funds to plan for your daughter higher education needs (post-graduation expenses).

But to earn respectable returns, selection is the key!

You need to own and hold the right type and sub-category of mutual fund schemes, so that the investment portfolio is well-strategized in line with your risk profile, the investment objective, the financial goal, and the time horizon to fulfil your financial goal.

In your case, you have a sufficient time horizon of over 15 years to go before the financial goal needs to be achieved (your daughter's higher education expenses). And assuming you can afford to take the high risk (backed by your financial health and circumstances), equity-oriented mutual funds can be an appropriate choice.

Equity-oriented mutual funds invest a dominant portion of their assets in equity and equity related instruments. Broadly, the investment objective of an equity-oriented mutual fund is to generate capital appreciation over the long term.

To plan for long-term financial goals and clock effective inflation-adjusted returns (also known as the real rate of returns), equity-oriented mutual funds are an appropriate choice.

As per the capital market regulator's diktat on mutual fund re-categorization, there are 10 sub-categories of equity mutual funds:

-

Large-cap Fund

-

Large & Midcap Fund

-

Midcap Fund

-

Small-cap Fund

-

Multi-cap Fund

-

Dividend Yield Fund

-

Value/Contra Fund

-

Focused Fund

-

Sectoral/Thematic Fund

-

ELSS (Equity Linked Savings Scheme)

Each of the above has distinct characteristics - these are defined by the regulator. Every type of equity-oriented mutual fund carries a distinct risk-reward relationship. To understand the trait of each one, download PersonalFN's Money Simplified Guide: Understanding Mutual Funds -- Equity, Debt, and Gold ...it is an extremely valuable resource.

[Read: How To Be Mindful While Planning For Your Child's Future?]

Indicatively, when you have a longer investment time horizon, the portfolio can be inclined to equity. But as you progress nearer to the goal over time, the allocation towards equity should gradually reduce and money should be parked in debt & money market mutual funds and/or bank Fixed Deposits. A portion of your total investible surplus can be held in gold, as a portfolio diversifier and hedge.

Similarly, there are solution-oriented schemes, known as Children's Funds to address goals such as your child's future needs.

Children's Funds have a lock-in of 5 years or until the child attains the age of majority (18 years), whichever is earlier. So, given the lock-in of 5 years, you need to carefully assess your liquidity needs-as to when you need money to fulfil the goal. Remember you will not be able to switch to another worthy scheme if the solution-oriented scheme underperforms.

The approach to follow when you are addressing a long-term financial goal...

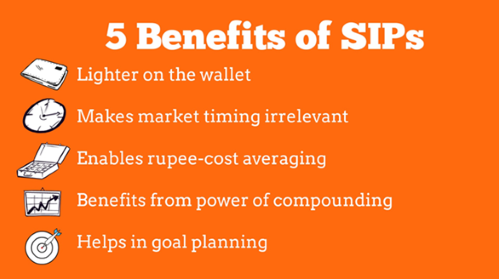

Systematic Investment Plans (SIPs), a mode of investing in mutual funds), can prove to be a rewarding strategy to accomplish your financial goals.

SIP has made life easy--it's lighter on the wallet, and you don't need to time the market to generate wealth while you endeavour to compound wealth. The rupee-cost averaging feature of SIP helps you mitigate the volatility of the equity market.

[Read: Best SIPs To Invest in 2019]

In order for the path to wealth creation to continue unhindered, ensure you do not stop or discontinue your SIPs in between, as far as possible. The tenure of your SIPs in equity mutual funds should be longer, in line with the investment horizon set for your envisioned financial goals.

Furthermore, when you invest, opt for Direct Plans over Regular Plans. The lower expense ratio of Direct Plans can add significant additional returns to your portfolio in the long run.

Mutual funds are a promising investment avenue for wealth creation. But avoid basing your investment decision solely on the returns aspect. You need to recognise the risk involved.

[Read: Why Comparing Returns to Risk Is More Meaningful!]

"Education is the most powerful weapon which you can use to change the world." - Nelson Mandela.

Have a question related to Mutual Funds? Ask PersonalFN Now!

© Quantum Information Services Pvt. Ltd. All rights reserved.

Any act of copying, reproducing or distributing this report whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: The information provided herein does not constitute to an Investment Advice/Fund Recommendation. This does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. PersonalFN and its subsidiaries / affiliates / sponsors / trustee or their officers, employees, personnel, directors will not be responsible for any direct/indirect loss or liability incurred by the user as a consequence of his or any other person on his behalf taking any investment decisions based on the contents provided herein. The user must make his/her own investment decisions based on his/her specific investment objective and financial position and using such independent advisors as he/she believes necessary. PersonalFN does not warrant completeness or accuracy of any information published herein. All intellectual property rights emerging from this content are and shall remain with PersonalFN. This is not directed for access or use by anyone in a country, especially USA or Canada, where such use or access is unlawful or which may subject PersonalFN or its affiliates to any registration or licensing requirement. This is a generalized Service, provided on an "As Is" basis by PersonalFN. Past performance is not a guide for future performance. As a condition to accessing PersonalFN content and website, you agree to our Terms and Conditions of Use.

Mutual Fund investments are subject to market risk. Please read the offer document carefully before investing.

Add Comments

| Comments |

kahmed963@gmail.com

May 08, 2019

Good learn but........ |

1